Archive

Growth and Concentration in the French-language Network Media Economy in Canada, 2000-2012

Cross posted from the Canadian Media Concentration Research Project website.

This post focuses on the development of and concentration trends in eight sectors of the network media economy in French-language regions of Canada from 2000 until 2012: i.e. wireline telecoms, mobile wireless services, internet access, broadcast tv, pay and specialty tv channels, total tv, radio and online advertising. It is a follow up to previous posts that looked at these matters across Canada as a whole (see here and here for the last two)(for a downloadable PDF version of this post please click here).

As with the previous posts, the data and methodology underpinning the analysis in this post can be found through the following links: Media Industry Data, Sources and Explanatory Notes, French Media Economy, CR and HHI French Media and the CMCR Project’s Methodology Primary. Excellent additional resources for further analysis of the media in French-language regions of Canada can be found through the GRICIS research project at Université du Québec in Montreal and the Centre d’études sur les médias at Laval. Journalist Steve Faguy is also very knowledgeable about the media industries in Quebec.

So what did we find?

The Growth of the French-Language Network Media Economy, 2000-2012.

The media economy in French-language Canada has expanded greatly since 2000. Revenues rose from $9.8 billion to $14.5 billion in the last dozen years and, indeed, the French-language media grew faster than in the rest of Canada. The relatively fast pace of growth, however, has slowed considerably since the “great financial crisis” of 2008, just as has been the case with the rest of Canada and indeed for much of the Anglo European world,

The faster rate of growth relative to the rest of Canada likely reflects the fact that, historically the French-language media economy has been smaller than what its population alone would dictate. For instance, while Quebec’s population accounts for about 23% of the national total, in 2012 it’s media economy accounted for just over a fifth of the total Canadian media economy (20.6%) – although that was up from just 18% at the turn-of-the-century.

Figure 1 below shows the trends.

Figure 1: The Growth of the French-Language Network Media Economy, 2000-2012

Sources: French Media Economy, Sources and Explanatory Notes.

The fastest growing sectors of the French-language media economy, again similar to patterns in the rest of Canada, have been in internet advertising (2,442%), internet access (524%), mobile wireless services (237%), cable, satellite and IPTV (118%) and, less so, television (34%). By and large, it is the platform media industries and, again to a lesser extent, television that are driving the growth of the network media ecology, adding both to its size and structural complexity.

At the opposite end of the spectrum, wireline telecom has fallen by more than a quarter. Newspapers also saw their revenues decline after seeming to peak in 2008, from an estimated $1,036 million then to $907 billion last year – a drop of 12%.

While these trends areconsistent with the course of events in the rest of the country, and indeed throughout much of the Anglo European world, one important thing distinguishes French-language dailies form the rest of the country: paywalls. Unlike the English-language press where twenty-four dailies accounting for two-thirds of circulation have put up paywalls in a bid to stem the tide, only two dailies out of ten in Quebec representing just under half of average daily circulation – Quebecor’s Le Journal de Montréal and Le Journal de Québec – have done so.

Power Corporation’s La Presse has resisted the temptation. This difference in the extent to which English- and French-language dailies have embraced paywalls likely reflects the fact that Radio Canada/CBC looms larger in Quebec than elsewhere in Canada, and perhaps cultural considerations as well.

Radio has grown only modestly since 2000. In fact, since 2008, the medium has seen revenue stagnate, largely because of a combination of budget cuts and restraint in government funding of the CBC and flat advertising spend, with the latter largely being a function, once again, of the economic uncertainty since the financial crisis.

One more thing that stands out from Figure 1 is the extent to which the growth of several media flattens or goes into decline after the onset of the “great financial crisis” in 2008. Indeed, several sectors see a dogleg in growth at this time: cable, satellite and IPTV as well as internet access, notably. Even fast growing mobile wireless services slowed, while newspaper revenues dropped.

Figure 2 below gives a snapshot of these conditions based on trends since 2000.

Figure 2: Growth, Stagnation and Decline in the French-language Media Economy, 2000-2012.

Leading Telecoms, Media and Internet Companies in Quebec

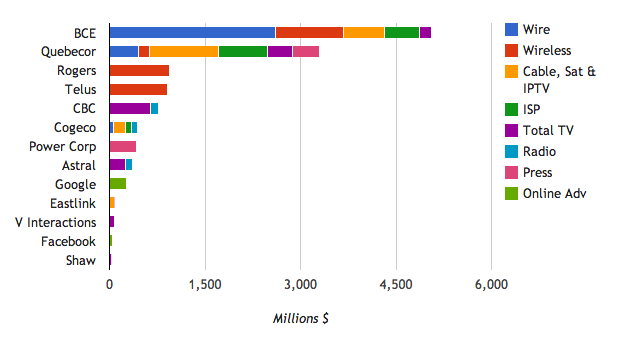

Every study of the Canadian media industries highlights the colossal role that Quebecor plays in French-language media, and rightly so. The company’s reach across the telecoms, television, newspaper, magazine, book and music retailing landscape is enormous. With over 80% of the sprawling media conglomerate’s $4 billion in revenues — $3.3 billion — coming from Quebec in 2012,[i] the company single-handedly accounts for over one-fifth of all French-language network media economy revenue.

While Quebecor no doubt cuts an imposing figure within French-language media, it is not the largest media conglomerate in this respect; Bell is — by a large margin. Figure 3 illustrates the point and shows the top 14 companies and their revenues from the eight sectors canvassed in this post. Figure 4 immediately after that shows what conditions would have looked like if the CRTC had approved Bell Astral Version 1.0.

Figure 3: Leading Media, Internet and Telecoms Companies in Quebec, 2012 (millions$).

Figure 4: Leading Media, Internet and Telecoms Companies in Quebec, 2012 (millions$) — Post Bell Astral Version 1.0

Sources: Media Industry Data, French Media Economy, Sources and Explanatory Notes.

Several interesting points stand out from Figure 3. First, taking all their holdings into account in Quebec, Bell’s 2012 revenues of just over $5 billion outstripped Quebecor’s $3.3 billion by a large margin. In fact, BCE accounted for more than a third of all revenue in Quebec, which was roughly equal to the next three biggest players combined: Quebecor, Rogers and Telus.

If the CRTC had approved the 2012 version of Bell’s bid to take-over Astral, as Figure 4 illustrates, the gap would be larger yet. Under the first version of that failed transaction, BCE’s total share of the French network media economy would have been 37.2% versus 22.6% for Quebecor (the consequences of the Competition Bureau and CRTC’s approval of Bell’s revised bid to acquire Astral in early 2013 will be discussed in next year’s post when the effects based on 2013 data will be discernible).

As Figures 3 and 4 show, Bell and Quebecor are in a league of their own. The two vertically-integrated giants tower over their peers, most of whom operate in only one or two sectors. Cogeco is a partial exception because it too is vertically integrated because of its stakes in high-speed internet access, basic phone service, cable tv and radio, but its revenue ($445 million) and market share (3.1%) across the ‘total network media economy’ are puny by the standards of Bell or Quebecor.

Joining Cogeco are another half-dozen or so second tier players: Rogers, Telus, the CBC, Power Corp, Astral and Google with French-language media revenues in $200-$950 million range. Telus and Rogers’ stakes in Quebec are mostly limited to mobile wireless services, although the size of the mobile wireless segment, and the fact that after internet advertising and internet access, it is the fastest growing sector, means that the two comapnies loom large in the province. Google is ranked ninth based on estimated revenues of $268.4 million from online advertising in 2012 and just under two percent share of the entire network media economy (versus $242.2 million in 2011).

The CBC still cuts a formidable presence in the province as well. Indeed, it is the largest player in TV and radio, with a 40% and one-third share of both media markets, respectively, compared to Quebecor with one-quarter of the French tv market and Astral’s 27% of the radio market in 2012. The CBC/Radio Canada’s major role is probably one reason, as mentioned earlier, why the French-language press has been more hesitant to introduce paywalls, as noted above; it is also why the CBC is so vilified by Quebecor and others in the English-language press.

Power Corps’ place as the seventh largest media enterprise in French-language markets gives a sense of the continued importance of the press within the overall mediascape and of the scale of its newspaper interests (i.e. La Presse, Le Nouvelliste, La Tribune, La Voix de l’Est, Le Soleil, Le Quotidien, Le Droit). Power Corp’s share of average daily circulation is equal to that of Quebecor’s two French-language dailies, Le Journal de Montréal and Le Journal de Québec: 47% — the basis which I use to estimate newspaper revenues for both companies in French-language markets. Independents pick up the remaining six percent of the circulation and revenues.

The French-language newspaper market, in short, is extremely concentrated, and more so than the national situation. Given the importance of newspapers amongst political and business elites, it is this dominance that no doubt draws a critical eye to both companies, and especially to Quebecor given it’s sprawling grasp across media, while Bell’s relative absence from ‘opinion influencing media’ seem to give it a freer hand in this regard.

Finally, a number of smaller players with less than one percent market share round out the ranks: Eastlink (.7% market share), V Interactions (.5%), Facebook (.2%) and Shaw (.2%). Together these four companies account for less than two percent market share.

Concentration in the French-language Network Media Economy, 2000-2012

Beyond the individual companies and their ranking, the most notable point with respect to the French-language media is the extent to which just two entities — BCE and Quebecor – dominate the landscape. Together, they account for well over half of all revenues (57%) (BCE’s market share in 2012 was 34.7%; Quebecor’s 22.6%). And this was before the Competition Bureau and CRTC blessed BCE’s take-over of Astral, the 8th largest French-language media company, earlier this year.

The second observation to be made is that concentration trends across the board are considerably higher for French-language media markets than in their national counterparts, except wireless. This is important for several reasons.

For one, it shows that the national measure we rely most on can be insensitive to conditions on the ground at the local/regional level. To put this more bluntly, we under-estimate concentration levels, not exagerrate them. This in turn makes the case that there is a media concentration problem in Canada even stronger.

Table 1, below, depict the trends over time in French-language network media economy on the basis of two standards methods for analyzing concentration: Concentration Ratios (CR4) and the Herfindhahl – Hirschman Index (HHI) (see methodology discussion in the last post and the CMCR project’s methodology primer).

Tables 1: CR and HHI Scores for the French-language Media Economy, 2000-2012

Sources: CMCR Project CR and HHI French Media.

Table 1 shows that every single sector of the media, telecom and internet examined here is very highly concentrated in Quebec, except for radio which slipped under the threshold for the designation in 2012.

The Platform Media Industries

One notable trend moving gradually in the opposite direction is the steady decline in the extremely high levels of concentration in mobile wireless services. One thing that stands out in this regard is that Quebecor has emerged as a significant rival to Bell (33% market share), Rogers (29%) and Telus (28%) since entering the market after acquiring spectrum in the last round of spectrum auctions in Canada in 2008.

Quebecor’s share of the market has grown to 5.3% (based on revenues) in the four years since it entered the market, effectively demonstrating the viability of the 4th player strategy. Other newcomers, notably Wind, have picked up about 4.7% market share, as well. As a result, Quebecor, Wind and other newcomers now account for 10% of the market, while the big three’s share has dropped to 90% since 2008. While the mobile wireless market is still highly concentrated by the CR4 (95.3%) and HHI (2742) measures, Quebec stands out as (1) the province with the highest levels of competition and (2) indicating the viability of a “4th mobile wireless carrier” strategy.

In contrast, a less unusual trend can be seen when we turn our attention to internet access. In this case, the levels of concentration are much higher in Quebec than they are across the country. Indeed, concentration levels for internet access have risen steadily and sharply since 2008, reaching an HHI of 2726 in 2012, a score that is firmly in the very concentrated zone versus one that was more in the moderately concentrated region just four years earlier. The CR4 in 2012 was also high at 78%.

In contrast, Canada-wide, the CR4 was 59% and the HHI at the low end of the scale at 1051. It is the former measure that is the more accurate, though, while the gap between them a reflection of measuring things nationally despite the fact that access to the internet is arranged in light of the choices available locally. Both measures are useful, though, and this why we look at things from multiple angles.

In terms of the broadcast distribution markets (BDUs), IPTV services have steadily grown to become more significant rivals to incumbent cable and DTH companies since 2010. The CR4 and HHI scores both fell slightly between 2011 and 2012, but are still at the extremely concentrated levels they were two years earlier: CR4 = 91.5%; HHI = 3400.

Concentration has hardly budged over the past few years. In 2012, Quebecor and BCE accounted for 49.3% and 29.5% market share, respectively, or just shy of four-fifths of the BDU market. The big two have increasingly clashed over the past twelve years, however, as BCE’s share of the market nearly tripled, rising from 10% to 30%, while Quebecor’s slid from 65% in 2000 to just under 50% in 2012.

A key reason why concentration remains sky high in Quebec is that BCE began rolling out IPTV services in 2010, half-a-decade later than in the prairie provinces, and did so in a way designed to protect its investments in DTH satellite TV. Cogeco and Eastlink remain distant rivals behind the big two, with 9% and 3.5% market share respectively.

Figure 5: Cable, DTH & IPTV French-Language Market Share, 2012

Sources: French Media Economy, Sources and Explanatory Notes.

Sources: French Media Economy, Sources and Explanatory Notes.

The Content Media Industries

Casting the net a bit more broadly to bring television into view alongside the distribution side of this domain also illustrates the extent to which Quebecor and Bell, and their strategies of vertical integration, stand apart from the rest of the field by a very wide margin. As Figure 5 below illustrates, the “big two” account for about two-thirds of the total tv universe, including distribution platforms. The CR4 for this measure is just shy of 82%, while an HHI of 2377 puts it just under the threshold for highly concentrated markets.

Again, it is worthwhile to reiterate that such claims are based on 2012 data before consolidation increased yet further on account of Bell’s take-over of Astral Media. Figure 6 illustrates the state of affairs with respect to BDU and the total television market in Quebec as of 2012.

Figure 6: Vertically-Integrated BDUs and Total Television by French-Language Market Share, 2012

Sources: French Media Economy, Sources and Explanatory Notes.

French-language broadcast television consists of three main players: CBC/Radio Canada (60% market share), Quebecor/TVA (27.3%) and V Interactions (7.8%). Broadcast television is extremely concentrated with the top 3 players accounting for 95$% of revenues and a sky-high HHI of 4403. Bell has no interests in this segment, and did not acquire any either when taking over Astral.

Radio is not nearly as concentrated, but still sits at the high-end of the moderately concentrated spectrum with an HHI of 2407 and a CR3 of 84%. Once again, the biggest player on the radio landscape is the CBC/Radio Canada, with a third of all revenues. Astral was the top commercial radio broadcaster and 2nd after Radio Canada and ahead of Cogeco in 2012 with 27%. Big 3 control 84.1% of radio, and the sector fell just under the threshold of highly concentrated in 2012 based on an HHI score 2407. The biggest change in recent years was Shaw (Corus) exit from French-language radio in 2011 after a radio station swap with Cogeco.

The trend for French language pay and specialty TV services is followed a U-shaped pattern over the decade, with concentration declining between 2004 and 2010, but rising again after 2010. Despite the half-a-decade or so dip, this sector has always remained highly concentrated on both the CR4 and HHI measures, with the “big four” – Astral, BCE, Quebecor and the CBC – accounting for 95.3% of revenues in 2012, and an HHI score of 2670.

Bell was already the second largest player in specialty and pay tv services in 2012 with a 27.1% market share. It would have single-handedly held an extraordinary two-thirds (64.8%) of the market had its original bid for Astral Media — the biggest player in this sector — been given the green light by the CRTC in 2012. The CR4 would also have risen from 95.3% to 99.3%, and the HHI score soared to 4,715. While the outcomes from the 2013 Bell Astral transaction will be assessed in next year’s version of this post, the difference is a matter of slight degree, not in kind: the results are off-the–charts in terms of CR4 and HHI guidelines.

In 2012, the total French-language TV market was highly concentrated by either the CR4 (92%) or the HHI (2594). The biggest entity is still Radio Canada, with 40% market share, trailed by Quebecor (TVA)(24%), Astral (16%) and Bell (11%). Had Bell’s original proposal to acquire Astral been approved as planned without any divestitures, its market share would have risen sharply from 11.1% to 27.7% and the third largest player, Astral, would have disappeared.

Concluding Thoughts

Studying the media industries and their evolution over time is never easy, and it becomes more difficult the deeper one probes simply because so much data is not released to scholars or the public. However, based on what we do know and some reasonable estimates of revenues and market shares derived from that, we can arrive at a pretty detailed and reasonable portrait of the French-language network media economy.

And in this regard, several things stand out.

- the French-language media economy is very concentrated and much more so than the Canadian media economy as a whole.

- Bell is the largest player in French-language markets with over one-third of all revenues across a wide swathe of media, followed by Quebecor with just under a quarter of the market across an equally large span of media, telecom and internet markets. The two are in a league of their own.

- The market shares of BCE and Quebecor are significantly larger within Quebec than they are on the national stage (e.g. for Bell, its total share of the French-language market is 35%, while nationally it is 28%; for Quebecor, the gap is more pronounced, with 23% of all revenues in Quebec versus a modest 6% at the national level).

- Similar patterns are observable in terms of the structure of the network media economy as a whole, with an HHI of 1800 in the French-language media being 400 points higher than what it is at the national level.

- Two important exceptions to this general portrait need to be made. First, radio nominally falls into the moderately concentrated zone. Second, the steady uptick in competition in wireless bodes well for those who suggest that a fourth wireless competitor strategy might be just what is needed to help the ailing mobile wireless sector in Canada, at least if international measures are our guide (see here, here, here and here)

[i] For the sectors covered by the CMCR project and not including music and books.

Media and Internet Concentration in Canada, 1984-2012

Reposted from the Canadian Media Concentration Research Project website (for a downloadable pdf version of this report please click here).

This is the second post in a series. Building on last week’s post that analyzed the growth of the media economy between 1984 and 2012, this post addresses a deceptively simple yet profound question: have telecom, media and internet (TMI) markets become more or less concentrated over the same period of time?

In Media Ownership and Concentration in America, Eli Noam (2009; also see 2013) notes that creating a coherent portrait of media concentration is difficult. Strong views are plentiful, but good evidence is not. Canadian scholar Philip Savage makes much the same observation, noting that debates over media concentration in Canada “largely occur in a vacuum, lacking evidence to ground arguments or potential policy creation either way”.

This post addresses that gap by providing a long-term, systematic, data-driven analysis of concentration trends across a dozen or sectors in Canada for the years between 1984 and 2012: wireline and wireless telecoms, internet access, BDUs (cable, satellite & IPTV), specialty and pay TV, broadcast TV, radio, newspapers, magazines, search engines, social media sites, online news sources, browsers and smart phone operating systems. These are the essential elements of the network media economy.

Concentration trends are assessed sector-by-sector and then across the network media as a whole using two common analytical tools — concentration ratios (CR) and the Herfindahl – Hirschman Index (HHI). While we cite our sources below, by and large, the following documents and data sets underpin the analysis in this post: Media Industry Data, Sources and Explanatory Notes and the CMCR Project’s Methodology Primary.

Media Concentration: Contentious Debates, Main Issues

Some consider discussions of media concentration in the age of the internet to be ridiculous. Leonard Asper, the former CEO of bankrupt Canwest, quipped, “the media have become more fragmented than ever. People who think otherwise probably believe that Elvis is still alive”. Chris Dornan points to how a Senate report that came out in 2006 was written by a bunch of Senators with their heads buried in the sand.

In Bell Astral 2.0, BCE said that while many critics allege that concentration in Canada is high, the evidence, “regardless of the metric employed – proves otherwise” (Bell Reply, para 46). When there are thousands of websites, social networking sites galore, pro-am journalists, a cacophony of blogs, 744 TV channels licensed for distribution in Canada, ninety-five daily newspapers and smartphones in every pocket, how could media concentration possibly be a problem?

If there was ever a golden media age, this is it, argue Thierer & Eskelen, 2008. Media economics professor, Ben Compaine (2005) offers a terse one-word retort to anyone who thinks otherwise: Internet.

Shackling media companies with ownership restrictions when they face global digital media giants like Google, Amazon, Netflix, Facebook, and so on is to condemn them to a slow death by strangulation (Skorup & Thierer, 2012; Dornan, 2012). Journalist’s too often share this view mostly, it seems, because they rely on industry insiders while considering balance and objectivity to be achieved when two industry insiders are shown to disagree with one another.

Critics, in contrast, tend to see media concentration as steadily going from bad to worse. Ben Bagdikian, for instance, claims that the number of media firms in the US that account for the majority of revenues plunged from 50 in 1984 to just five by the mid-2000s. Canadian critics decry the debasement of news and the political climate of the country (here and here). Others see internet as another frontier of capitalist colonization and monopolization (Foster & McChesney, 2012).

A third school of scholars aims to detect the influence of changes of media ownership and consolidation by quantitatively analyzing reams of media content. They generally find that the evidence is “mixed and inconclusive” (here). The newest of such studies, Cross-Media Ownership and Democratic Practice in Canada: Content-Sharing and the Impact of New Media, comes to similar conclusions (Soderlund, Brin, Miljan & Hildebrandt, 2011).

Such findings, however, proceeds as if ‘impact on content’ is the only concern, or as Todd Gitlin put in many years ago, as if ‘no effect’ might not be better interpreted as preserving the status quo and thus a significant problem in its own right.

A fourth school of thought, and one that I largely subscribe to, sees the shift from the industrial media of the 19th and 20th centuries to the online digital media of the 21st century as entailing enormous changes. However, it also argues that these changes also entail an equally enormous “battle over the institutional ecology of the digital environment” (Benkler, 2006, ch. 11). The history of human communication is one of recurring ‘monopolies of knowledge” (Innis, 1951) and oscillations between consolidation and competition (John, 2010; Babe, 1990), so why should we expect this to be any less true today(Noam, 2009; Benkler, 2006; Wu, 2010; Crawford, 2012)?

As Noam (2013) states after reflecting on the results of a thirty-country study, concentration around the world is “astonishingly high”. Whether Canada ranks high by international standards, low or in between will be dealt with in a subsequent post.

The core elements of the networked digital media – e.g. wireless (Rogers, BCE, Telus), search engines (Google), Internet access (ISPs), music and book retailing (Apple and Amazon), social media (Facebook) and access devices (Apple, Google, Nokia, Samsung) – may actually be more prone to concentration because digitization magnifies economies of scale and network effects in some areas, while reducing barriers in others, thereby allowing many small players to flourish. A two-tiered digital media system may be emerging, with numerous small niche players revolving around a few enormous “integrator firms” at the centre (Noam, 2009; Wu, 2010).

All this matters because the more core elements of the networked media are concentrated, the easier it is for dominant players to exercise market power, coordinate behaviour, preserve their entrenched stakes in ‘legacy’ media sectors (e.g. television and film), stifle innovation, influence prices and work against market forces and the needs of consumers and citizens (see here, here, here, here and here). Large consolidated telecom, media and internet giants also make juicy targets for those who would turn them into proxies working on behalf of the copyright industries, efforts to block pornography, and as part of the machinery of law enforcement and national security (see here, here and here).

In sum, the more concentrated the digital media giants are, the greater their power to:

- set the terms for the distribution of income to musicians, journalists and media workers, and authors (Google, Apple, Amazon);

- turn market power into moral authority by regulating what content can be distributed via their ‘walled gardens’ (Apple);

- set the terms for owning, controlling, syndicating and selling advertising around user created content (Google, Facebook, Twitter) (van Couvering, 2011; Fuchs, 2011);

- use media outlets they own in one area to promote their interests in another (see Telus intervention in Bell Astral, 2.0 pages 4-6 and here);

- and set defacto corporate policy norms governing the collection, retention and disclosure of personal information to commercial and government third parties.

Whilst we must adjust our analysis to new realities, long-standing concerns remain as well. Consider, for example, the fact that every newspaper in Canada, except the Toronto Star, that editorially endorsed a candidate for Prime Minister in the 2011 federal election touted Harper –three times his standing in opinion polls at the time and the results of the prior election.

Ultimately, talk about media concentration is really a proxy for conversations about consumer choice, freedom of the press and democracy. Of course, such discussions must adapt to changes in the techno-economic environment of the media but the advent of digital media does not render them irrelevant (Baker, 2007; Noam, 2009; Peters, 1999).

Methodology

Measuring media concentration begins by defining the media studied, as noted at the outset. I then collected revenue data for each of these sectors and for each of the firms within them with over a one percent market share. This handy dandy list of sources and others listed here were used.

Each media is analyzed on its own and then grouped into three categories, before scaffolding upward to get a birds-eye view of the entire network media ecology: (1) platform media; (2) content media: (3) online media. The results are analyzed over time from 1984 to 2012. Lastly, two common tools — Concentration Ratios (CR) and the Herfindhahl – Hirschman Index (HHI) – are used to depict levels of concentration and trends over time within each sector and across the network media ecology as a whole.

The CR method adds the shares of each firm in a market and makes judgments based on widely accepted standards, with four firms (CR4) having more than 50 percent market share and 8 firms (CR8) more than 75 percent considered to be indicators of media concentration (see Albarran, p. 48). The Competition Bureau uses a more relaxed standard, with a CR4 of 65% or more possibly leading to a deal being reviewed to see if it “would likely . . . lessen competition substantially” (p. 19, fn 31).

The HHI method squares and sums the market share of each firm in a market to arrive at a total. If there are 100 firms, each with a 1% market share, then markets are highly competitive, while a monopoly prevails when a single firm has 100% market share. The US Department of Justice set out new guidelines in 2010 for determining when concentration is likely to exist, with the new thresholds set as follow:

HHI < 1500 Unconcentrated

HHI > 1500 but < 2,500 Moderately Concentrated

HHI > 2,500 Highly Concentrated

At first blush, these higher thresholds seem to water down the earlier standards that had been set at lower levels and used since 1992. The new guidelines, however, are probably even more sensitive to reality and tougher than the ones they supersede.

This is because they go beyond setting thresholds to give more emphasis to the degree of change in market power. For instance, “mergers resulting in highly concentrated markets that involve an increase in the HHI of more than 200 points will be presumed to be likely to enhance market power”, observes the DOJ (emphasis added, p. 19).

Second, markets are defined precisely based on geography and the relevant details of the good at hand versus loose amalgamations of things that are based only on superficially similarities. This is critical, and it distinguishes those who would define the media universe so broadly as to put photocopiers and chip makers alongside ISPs, newspapers, film and TV and call the whole thing “the media” versus the ‘scaffolding approach’ we use that starts by analyzing each sector before moving up to higher levels of generality from there until reaching a birds-eye perspective on the network media as a whole.

Third, the new guidelines also turn a circumspect eye on claims that enhanced market power will be good for consumers and citizens because they will benefit from the increased efficiencies that result. What is good for companies is not necessarily good for the country (see Stucke & Grunes, 2012).

Lastly, the new guidelines are emphatic that decisions turn on “what will likely happen . . . and that certainty about anticompetitive effect is seldom possible and not required for a merger to be illegal” (p. 1). In practice this means that the goal is to nip potential problems in the bud before they occur; to “interdict competitive problems in their incipiency”, as the guidelines say (p. 1). Crucially, this means that experience, the best available evidence, contemporary and historical analogies as well as reasonable economic theories are the basis of judgment, not deference to impossible (and implacable) demands for infallible proof (p. 1).

These assumptions overturn a quarter-century of economic orthodoxy and its grip on thinking about market concentration (see Stucke & Grunes, 2012 and Posner). Freed from the straight-jacket of Chicago School economic orthodoxy, and the subordination of policies and politics to economists and judges, the new guidelines set a tough hurdle for those with the urge to merge. It was precisely this kind of thinking that killed the bid by AT&T – the second largest mobile wireless company in the US – to acquire the fourth largest, T-Mobile, in 2011, for instance (also Stucke & Grunes, 2012).

In Canada, in contrast, the CRTC Diversity of Voices sets up thresholds for a broadly defined TV market in which a proposed deal that results in a single owner having less than 35% of the total TV market will be given the green light; those that fall in the 35-45% range might be reviewed; anything over 45% will be rejected (para 87). Unlike the Competition Bureau that uses the CR4 method whereby a deal that result in a CR4 over 65% may be reviewed to determine whether it will substantially lessen competition, the CRTC has no such guidelines, although a recent accord between the two regulators might change this.

The CRTC’s threshold for TV, instead, is based on a single snapshot of a single company’s share of one broadly defined market – the total TV market –“before” and “after” a single transaction. It is a static measure that has no sense of trends over time, the relational structure of markets or any capacity to analyze the drift of events across media and the network media ecology as a whole.

The Competition Bureau draws selectively from the US HHI guidelines. It does not use the HHI thresholds. Instead, it focuses on “the relative change in concentration before and after a merger” (emphasis added, p. 19, fn 31). How faithful it is to either its CR4 guidelines or the HHI criteria for judging relative changes in market power is open to question, however, in light of its decision earlier this year to bless Bell-Astral 2.0 (here). In Canada regulators appear to mostly make it up as they go along rather than consistently follow a coherent set of guidelines.

The Historical Record and Renewed Interest in Media Concentration in the 21st Century

There has always been keen interest in media ownership and concentration in Canada and the world since the late-19th and early-20th centuries.

In 1910, for example, the Board of Railway Commissioners (BRC) broke up the three-way alliance between the two biggest telegraph companies — Canadian Pacific Telegraph Co. and the Great Northwestern Telegraph Co. (the latter an arm of the New York-based goliath, Western Union) – and the American-based Associated Press news wire service. Why?

The BRC did this because, it argued, in the face of much corporate bluster, that allowing the telegraph companies to give away the AP news service for free to the leading newspaper in one city after another might be good for the companies but it would “put out of business every news-gathering agency that dared to enter the field of competition with them” (1910, p. 275). In a conscious bid to use telecoms regulation to foster the development of rival news agencies and newspapers, the BRC forced Western Union and CP Telegraphs to unbundle the AP news wire service from the underlying telegraph service. It was a huge victory for the Winnipeg-based Western Associated Press – which initiated the case – and other ‘new entrants’ into the daily newspaper business (Babe, 1990).

Media concentration issues came to a head again in the 1970s and beginning of the 1980s, when three inquiries were held: (1) the Special Senate Committee on Mass Media, The Uncertain Mirror (2 vols.)(Canada, 1970); (2) the Royal Commission on Corporate Concentration (1978); and (3) the Royal Commission on Newspapers (Canada, 1981).

Things lay dormant for more than two decades thereafter before springing to life again after a huge wave of consolidation in the late-1990s and turn-of-the-21st century thrust concerns with media concentration back into the spotlight. Three inquiries between 2003 and 2008 were held as a result: (1) the Standing Committee on Canadian Heritage, Our Cultural Sovereignty (2003); (2) the Standing Senate Committee on Transport and Communications, Final Report on the Canadian News Media (2006); (3) the CRTC’s Diversity of Voices report in 2008.

Competitive Openings and Two (three?) Waves of TMI Consolidation

As I noted in my last post, the media economy in Canada grew immensely from $39 billion in 1984 to $73.3 billion last year (in inflation-adjusted “2012 real dollars”). Between 1984 and 1996, new players meant more diversity in all sectors, except for newspapers as well as cable and satellite video distribution. Concentration climbed significantly in both of those sectors.

Conventional as well as pay and subscription television channels expanded during this time as well. In terms of ownership, incumbents and a few newcomers – e.g. Allarcom and Netstar –cultivated the field, with their share of the market growing steadily.

Concentration levels remained very high in wired line telecoms in the 1980s and early 1990s, too. Mobile wireless telecoms services were developed by two incumbents, Bell and Rogers. As had been the case in many countries, telecoms competition moved slowly from the ends of the network into services and then network infrastructure, with real competition emerging in the late-1990s before the trend was reversed and concentration levels began to climb again, notably after the dot.com crash in late-2000.

In the 1980s and early-1990s, consolidation took place mostly among players in single sectors. Conrad Black’s take-over of Southam newspapers in 1996 symbolized the times. In broadcast television, amalgamation amongst local ownership groups created the large national companies that came to single-handedly own the national commercial television networks by the end of the 1990s: CTV, Global, TVA, CHUM, TQS.

While weighty in their own right, these amalgamations did not have a big impact across the media. The CBC remained prominent, but public television was being eclipsed by commercial television as the CBC’s share of all resources in the television ‘system’ slid from 46 percent in 1984 to less than half that amount today (20.4%).

Gradual change defined the 1980s and early-1990s, but things shifted abruptly by the mid-1990s and into the 21st century as two (and maybe three) waves of consolidation swept across the TMI industries. A few highlights help to illustrate the trend:

Wave 1 – 1994 to 2000: Rogers’ acquisition of Maclean-Hunter (1994), but peaking from 1998 to 2001: (1) BCE acquires CTV and the Globe & Mail ($2.3b); (2) Quebecor takes over Videotron, TVA and the Sun newspaper chain ($ 7.4b) (1997-2000); (3) Canwest buys Global TV ($800m) and Hollinger newspapers papers, including National Post ($3.2b).

Wave 2 – 2006-2007. Bell Globe Media re-branded CTVglobemedia, as BCE exits media business. CTVglobemedia acquires CHUM assets (Much Music, City TV channels and A-Channel). CRTC requires CTVglobemedia to sell City TV stations – acquired by Rogers (2007). Astral Media’s buys Standard Broadcasting. Quebecor acquires Osprey Media (mid-size newspaper chain)(2006). Canwest, with Goldman Sachs, buys Alliance Atlantis (2007) (Showcase, National Geographic, HGTV, BBC Canada, etc) – and the biggest film distributor in Canada.

Wave 3 – 2010 – ? Canwest bankrupt. Newspapers acquired by Postmedia, TV assets by Shaw. BCE makes a comeback, buys CTV (2011) and bids for Astral Media in 2012, but fails to gain CRTC approval.

The massive influx of capital investment that drove these waves of consolidation across the telecom, media and Internet industries is illustrated in Figure 1 below.

Figure 1: Mergers and Acquisitions in Media and Telecoms, 1984–2012 (Mill$)

Sources: Thomson Reuters. Dataset on file with author.

Mergers and acquisitions rose sharply between 1994-1996, and spiked to unprecedented levels by 2000. The collapse of the TMT bubble ended such trends, until they restarted again between 2003 and 2007 before being ground to a halt by the Global Financial Crisis (2007ff), and with only a tentative step up since. These patterns reveal that trends in the network media economy parallel the state of the economy in near lockstep fashion; they also closely track those in the US and globally.

Consolidation has yielded a specific type of media company at the centre of the network media ecology in Canada: i.e. the integrated media conglomerate. While popular in the late-1990s in many countries, many media conglomerates have since collapsed or been broken up (AOL Time Warner, AT&T, Vivendi, CBS-Viacom, and parts of NewsCorp, etc)(see, for example, Jin, 2011; Jin, 2013; Skorup & Thierer, 2012; Thierer & Eskelen, 2008; Waterman & Choi, 2010).

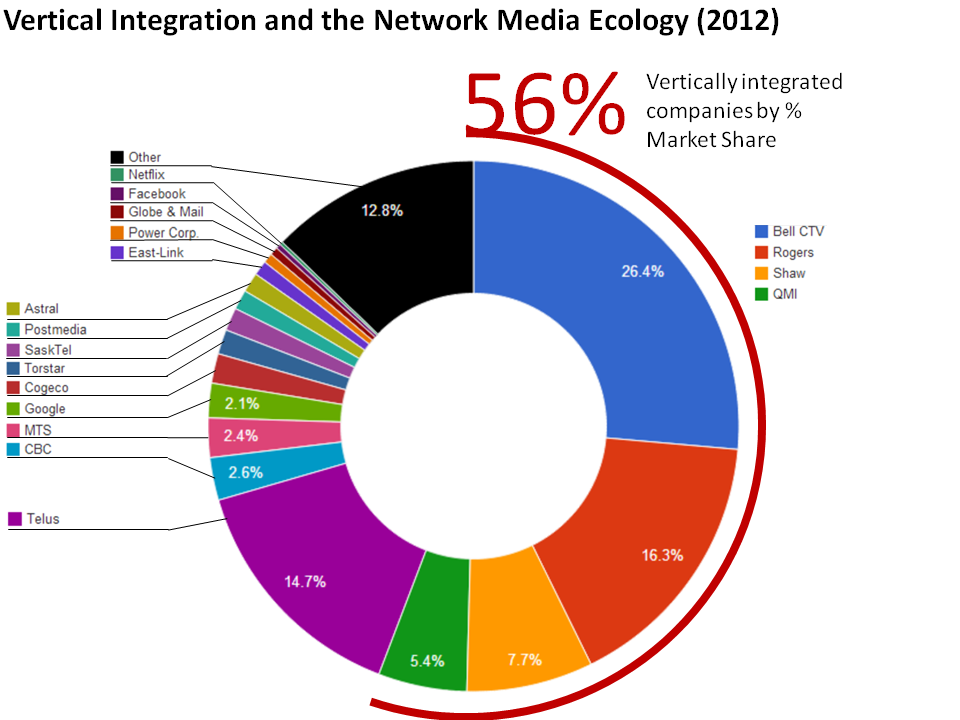

Despite deconvergence trends elsewhere, in Canada media-telecom and internet conglomerates are still all the rage. Figures 2 and 3, in fact, illustrate the acceleration of the trend toward vertical integration from 2008 to 2012, largely due to Shaw’s acquisition of the Global TV and a suite of specialty and pay TV channels from Canwest (2010) and Bells re-purchase of CTV (2011).

Figure 2:

Figure 3:

Sources: Media Industry Data, Sources and Explanatory Notes

By 2012, four giant vertically integrated TMI conglomerates accounted for 56% of all revenue across the network media economy: Bell (CTV), Rogers (CityTV), Shaw (Global) and QMI (TVA). Add Telus to the fold and the number swells to 71 percent. The ‘Big 5’ are joined by a second tier of a dozen or so more focused entities: the CBC, MTS, Google, Cogeco, Torstar, Sasktel, Postmedia, Astral, Eastlink, Power Corporation, the Globe and Mail, Facebook and Netflix, ranked on the basis of Canadian revenues.

Strip out the wireline and wireless telecoms sectors and we get a more sensitive view of what is going on across the rest of the media universe because those two sectors are so big that they cast a shadow over everything else. From this vantage point, the big ten’s share of revenue reached it’s low point in 1996 (51.7%), before reversing course to reach 58% in 2000. By 2004, the big four’s share of all revenues (without telecoms) soared to 70%, where things have stayed basically flat since. The big 10’s market share in 2012 was 69%: Bell, Shaw, Rogers, QMI CBC, Google, Cogeco, Torstar, Postmedia and Telus, in that order.

The big four’s share of the network media economy rose significantly to 48% in 2010 (after Shaw’s acquisition of Global) and rose again to 51% in 2011 (when Bell re-acquired CTV), where it has basically stayed since — an all-time high and well above the low point CR4 score of 24% in 1996. Media concentration in Canada is currently more than twice as high as in the US based on Noam’s analysis in Media Ownership and Concentration in America.

Figure 4 below depicts the relative share of the major players in the network media economy as things stood in 2012, without the telecommunications sectors.

Figure 4:

Sources: Media Industry Data, Sources and Explanatory Notes

The next section doubles back to look at things sector-by-sector, and within the three main categories in which we group these sectors:

- platform media (wireline & wireless, ISPs, cable, satellite, IPTV);

- ‘content’ (newspapers, tv, magazines, radio);

- ‘online media’ (search, social, operating systems).

At the end, I combine these again one last time to complete the analysis of the network media industries as whole.

Platform Media

All sectors of the platform media industries are highly concentrated or at the high-end of the moderately concentrated scale, and pretty much always have been, although Internet Access is a partial exception.

Table 1: CR and HHI Scores for the Platform Media Industries, 1984 – 2012

Sources: Media Industry Data and Sources and Explanatory Notes.

CR4 and HHI measures for wireline telecoms scores fell in the late-1990s as some competition took hold. They reached their lowest level ever at the time between 2000 and 2004 before the the dot.com bubble collapse took out many of the new rivals with it (CRTC, 2002, p. 21). Competition waned thereafter until 2008, but has risen since. Levels of concentration for this sector are very high nonetheless by both the CR4 and HHI measures.

Mobile Wireless

Much the same can be said with respect to wireless services. They have consistently been highly concentrated, and still are, despite the advent of four new entrants since 2008: Mobilicity, Wind Mobile, Public and Quebecor.

Some recent studies argue “that there is not a competition problem in mobile wireless services in Canada” (see here and here). That conclusion rests on questionable assertions about efficiencies are often asserted but seldom hold up under scrutiny and contestible markets theory in contrast to realities on the ground (see here, here and here).

Claims that there is no wireless competition problem in Canada clash with the reality that CR4 scores have been stuck in the ninety-percent range for the entire history of wireless in Canada, a level well-above the Competition Bureau’s standards. Concentration is a durable fixture in the wireless sector rather than something that will wilt over time. CR and HHI scores have drifted downwards since new rules to encourage new entrants were adopted for the spectrum auction in 2008, but in 2012 the HHI score was still 2873 – far above the 2,500 market that defines a highly concentrated market.

Two competitors – Clearnet and Microcell – emerged in the late-1990s and managed to garner 13.4 percent of the market between them, but were taken over by Telus and Rogers in 2000 and 2004, respectively. It is still too early to tell whether the new entrants will fare, but with only 7% market share in 2012 they were just half way to restoring the high-water mark of competition set a decade ago with mounting signs of trouble swirling about all of them, except Quebecor and, to a lesser extent, perhaps Wind – but these are points for next year’s post.

Internet Access

As the telecoms and Internet boom gathered steam in the latter half of the 1990s new players emerged to become significant competitors, with four companies taking over a third of the ISP market by 1996: AOL (12.1%), Istar, (7.2%), Hook-Up (7.2%) and Internet Direct (6.2 percent).

The early ‘competitive ISP era’, however, has yielded to more concentration since. Although the leading four ISPs accounted for a third of all revenues in 1996, by 2000 the big four’s (Bell, Shaw, Rogers & Quebecor) share had grown to 54 percent, where it stayed relatively steady for much of the rest of the decade. Since 2008, however, the CR4 has crawled upwards to reach 59% last year.

HHI scores for internet access doubled between 1996 and 2000, but are still low relative to most other sectors and to this measure’s standards for concentration. However, this reflects the limits of the HHI method in this case, since 93% of residential internet subscribers use one or another of the incumbent cable or telecom companies’ for internet access. The top 5 ISPs account for 76% of all residential high-speed internet access revenues (CRTC Communication Monitoring Report, pp. 143-144).

Climbing down from national measures to the local level, internet access is effectively a duopoly, with the left over 7% of the market not dominated by the incumbents scattered among 500 or so independent ISPs. TekSavvy is the biggest ISP with an estimated 180,000 subscribers in 2012 and just over 1% market share. Other small ISPs are on the wane (Primus). Indy ISPs’ market share has increased slightly from 2010, but it has stayed flat for the past two years and is nowhere near returning to the high-water mark of competitive internet access in the late-1990s.

Canada has relied on a framework of limited competition between incumbent telecom and cable companies for wireline, wireless, internet access and video distribution markets. Incumbents still dominate all of these sectors, while smaller rivals continue to eek out an existence on the margins in each.

Cable, Satellite and IPTV

Concentration in cable, satellite and IPTV distribution rose steadily from low levels in the 1980s (850) to the upper end of the moderately concentrated zone (by the new HHI guidelines) in 1996 (i.e. HHI=2300), before drifting downwards to the low 2000s by the turn-of-the-century. This is where things have stood until recently as the incumbent telcos’ IPTV services exert pressure on the incumbent cable companies.

The cable, satellite and IPTV industry is still largely a duopoly at the local level. The CR score has dropped 5% since 2004 but the big four still dominate with 81% market share: Shaw (25.1%), Rogers (22.3%), Bell (21.1%) and Quebecor (12.5%). Add the next five biggest players – Cogeco (7.5%), Eastlink (3.8%), Telus (3.6%), MTS (.9%) and SaskTel (.9) – and all but two percent of industry revenues are accounted for.

The telcos’ IPTV services are making incursions into the incumbent cable and satellite service providers’ turf, accounting for 7.5% of the TV distribution market by revenue in 2012 (based on my numbers, or about 6.7% percent using CRTC data)(see p. 110). In terms of subscribers, IPTV services account for 10% of the market (CRTC numbers are slightly lower, p. 111) (see here for partial explanation of the differences).

Since IPTV services began to be rolled out by MTS and SaskTel in 2004, followed later by Telus and Bell in 2008 and 2009, respectively, the HHI score has fallen 320 points (see Table 1 above) and now sits at the lower end of the “moderately concentrated” scale. The threat to incumbent cable companies is greatest in western Canada, where MTS, SaskTel and Telus have rolled out IPTV services faster than Bell from Ontario to the Atlantic.

Within the platform media industries as a whole, new players have emerged, but it is primarily the expansion of incumbent telcos and cable companies outside their traditional turf and into one anothers’ industries that is generating the greatest effect. There has been a modest increase in competition in all platform media sectors in recent years since except internet access. While new technologies have increased the structural complexity of platform media, they have not disrupted the long-standing trajectory of development when it comes to tv distribution: more channels, and a few new players, but with more of the whole in the hands of the old.

The Media Content Industries

Television

In the late 1980s until 1996, concentration in broadcast TV fell sharply while the specialty and pay TV channels emerging at this time displayed similarly high levels of competition. TV became much more diverse as a result.

Such trends abruptly reversed in the late-1990s, however, with something of a lag before the specialty and pay TV market began to follow suit. After the turn-of-the-century concentration levels for TV climbed steadily and substantially. The upswing since 2008 has been especially sharp. Figure 5, below, shows the trend in terms of CR scores; Figure 6, in terms of the HHI.

Figure 5 CR Scores for the Content Industries, 1984-2012

Figure 6 HHI Scores for the Content Industries, 1984-2012

Sources: Media Industry Data and Sources and Explanatory Notes.

In 2012, the largest four television providers controlled about 78% of all television revenues, up substantially from 71% four years earlier. In terms of the 700 TV channels actually operating in Canada, the big four own 171 of them in total and which account for just under four-fifths of all revenue: Shaw (66 tv channels), Bell (61), Rogers (24) and Quebecor (20). In contrast, in 2004, the big four accounted for 62% of the TV biz, a time before major players such as Alliance Atlantis and CHUM had carved out a significant place for themselves in the TV marketplace (circa 2000-2006), respectively.

Concentration across the total TV market has been pushed to new extremes in recent years, first, by Shaw’s take-over of Canwest’s television assets in 2010 and, second, by Bell’s buy-back of CTV the year after that. They would have been higher yet had the CRTC approved Bell’s acquisition of Astral Media – the fifth largest television provider – rising to about 86%. The about face on that matter in 2013 will be dealt within in next year’s version of this post.

In 2012 the largest four tv providers after Bell and Shaw are: the CBC, Rogers, Astral, and QMI, respectively, and in that order. Together, they accounted for 91% of the entire television industry last year. Similar patterns are replicated in each of the sub-components of the ‘total television’ measure (conventional television, pay and specialty channels), as the chart above illustrates.

In contrast, in 2004, the six largest players accounted for a little over three-quarters of all revenues. The run of HHI scores reinforces the view that the television industry is has become markedly more concentrated in the past two years.

CR and HHI measures for tv were the lowest in the 1990s when newcomers emerged (Netstar, Allarcom), yet before the time when the multiple ownership groups that had stood behind CTV and Global for decades combined into single groups. The period was significantly more diverse because the CBC no longer stood as the central pillar in tv and radio, while specialty and pay television channels were finally making their mark. Today, the latter are the jewel in the TV crown, but they are highly concentrated by the CR4 measure, with a CR4 of 81%, yet only moderately so by HHI standards with a score of 1906.

Newspapers

Concentration in the newspaper industry rose steadily from 1984 until 2008, when it peaked. In 1984, the top four groups accounted for 61% of all revenues, a number which had risen to about two-thirds of the market in 1996 – a level that stayed fairly steady for most of the next decade before rising again to an all-time high within the time frame studied here in 2008. At that point, the four largest newspaper groups accounted for three-quarters of the market: Canwest (23.7%), Quebecor (21.5%), Torstar (19.3%) and Power Corp (10.5%).

Levels have since declined considerably by either the CR4 or HHI measure, with the former falling to 69% in 2012 and the latter dropping from 1628 in 2008 to 1,398 – well within the ‘competitive’ range by the lights of the new HHI standards or only moderately concentrated by the old standards. The new conditions likely reflect Postmedia’s decision to sell some of its newspapers (Victoria Times Colonist) and to cut publishing schedules at others. Indeed, its market share has fallen steeply from 24% in 2008 when the papers were still in the hands of Canwest to just 17% last year, and within a significantly smaller market. A few new publishers have also emerged amidst the tough times now facing the newspaper industry, notably Black Publishing and Glacier Publishing in western Canada.

Magazines

Of all media sectors, magazines are least concentrated, with concentration levels falling by nearly one half on the basis of CR scores and two-thirds for the HHI over time.

Radio

Radio is also amongst the most diverse media sectors according to HHI scores, and only slightly concentrated by the C4 measure. The shuffling of several radio stations between Shaw/Corus and Cogeco in 2011 had continued the long-term decline in concentration, but in 2012 there was an uptick as the CR4 rose from 56% to 60% and the HHI from 954 to 1027. Bell’s take-over bid for Astral – Canada’s largest radio broadcaster – would have further pushed radio along this path had it have been approved by the CRTC in 2012. Levels of concentration would have been high by the CR measure, with the CR4 rising from 60% to 68%, but with an HHI of 1371 it would still have been well within the unconcentrated zone by the revised HHI guidelines or moderately concentrated by the old ones. .

Online Media

As the earlier discussion of internet access showed, there is little reason to believe that core elements of the Internet are immune to high levels of concentration. But what about other core elements of the Internet and digital media ecology: search engines, social media sites, browsers, operating systems and internet news sites?

Concentration in the search engine market grew markedly from 2004 to 2011. CR4 scores have been persistently sky-high during these years, rising from 93% in 2004 to almost 98% in 2011, while HHI scores have been off-the-charts in the 4000-7000 range. Google’s dominance seemed to be locked in the low 80%-range, with others lagging far behind, during this period.

Google’s share of search, however, tumbled in 2012 to just under 68%, although this still leaves Microsoft (17.8%), Yahoo! (5.4%), and Ask.com (6.2%) trailing far behind. The CR4 and HHI scores are still sky-high at 97% and 4995, respectively, and as Table 2 shows.

Table 2: CR4 and HHI Scores for the Search Engine Market, 2004-2012

Source: Experien Hitwise Canada. “Main Data Centre: Top 20 Sites & Engines.” last Accessed May 2013.

Social media sites display a similar but not quite as pronounced trend. Facebook accounted for 46% of unique visitors to such sites in December 2012, followed by Twitter (15%), LinkedIn (12%), Tumbler (12%), Instagram (9%) and Pinterest (6%) (Comscore). Again, the CR4 score of 85% and HHI score of 2762 reveal that social networking sites are highly concentrated.

Similar patterns hold for the top four web browsers in Canada. Microsoft’s Explorer (55%), Firefox (20%), Google’s Chrome (18%), Apple’s Safari (5%) have a market share of 98 percent (Netmarketshare). In terms of smart phone operating systems, the top four players accounted for 96 percent of revenues: Apple’s iOS (55%), Google’s Android OS (29%), Java (7%), Nokia’s Symbian (5%). RIM (3%) and Microsoft (1%) accounted for the rest (Netmarketshare).

Internet news sites are an exception to the extremely high levels of concentration in the online digital media environment. Internet users time on top 10 online news sites nearly doubled from 20 to 38 percent between 2003 and 2008. Most of that increased time is spent on sites that are extensions of well-known traditional media companies: cbc.ca, Quebecor, CTV, Globe & Mail, Radio Canada, Toronto Star, Post Media, Power Corp. Other major sources included CNN, BBC, Reuters, MSN, Google and Yahoo! (Zamaria & Fletcher, 2008, p. 176).

Despite this rapid “pooling of attention” on the top 15 or so news sites, concentration levels stayed flat between 2004 and 2007. They declined thereafter until 2011 – the latest year for which good data is available. Online news sources are not concentrated by either the CR or HHI measure and are diverse relative to any of the other sectors, except magazines.

Table 3: Internet News Sources, 2004-2011

Source: Table calculated by Fred Fletcher, York University, from the Canadian Internet Project Data sets (Charles Zamaria, Director). Reports on the 2004 and 2007 surveys are available at http://www.ciponline.ca.

The Network Media Industries as a Whole

Combining all the elements together yields a birds-eye view of long-term trends for the network media as a whole. Figure 7 below gives a snapshot of the state of the network media economy in 2012, listing those sectors that were unconcentrated, those that were moderately concentrated and finally those that were highly concentrated by HHI standards.

Figure 7: Concentration Rankings on the basis of HHI Scores, 2012

Clearly, things are not all to one side, with several sectors showing low levels of concentration. However, there is no shortage of segments where concentration is either moderately high or very high. Perhaps one of the most striking things to stand out from Figure 7 is the extent to which core elements of the internet and digital media ecology seem to be prone to very high levels of concentration.

Figures 8 and 9 show the trends over time on the basis of, first, CR1, CR4 and CR10 scores, followed by a depiction of the trends based on the HHI.

Figure 8: CR 4 Score for the Network Media Economy, 1984-2012

Sources: Media Industry Data and Sources and Explanatory Notes.

Looking the entirety of the network media economy, several distinct points emerge: The biggest company’s share of revenues across the whole of the media twenty-eight years ago was 48%; in 2012, it was 26.4% albeit in a vastly larger media universe. That company in 1984 was BCE; it is still the same company today, and substantially larger than the second and third ranked firms, Rogers and Shaw.

The CR4 levels today are about the same as they were twenty-eight years ago: 66.7% versus 65.1%. Today, the top 10 firms have a larger market share than they did in 1984: 81% versus 76%. These figures would have been higher had the CRTC given the green light to BCE’s first bid to acquire Astral in 2012, as Figure 8 shows.

Figure 9: HHI Scores for the Network Media Economy, 1984-2012

Sources: Media Industry Data and Sources and Explanatory Notes.

As Figure 9 shows, the HHI fell by half from 1984 to 2000. Trends then moved erratically for the next few years before stabilizing in the 1200 to 1300 range, before a significant step up in 2010 and with another potential step in the same direction last year before the CRTC nipped Bell’s bid to acquire Astral in the bud.

The results depict a competitive scenario by the revised 2010 HHI standards (or moderately concentrated by the old standards) – if we take the ‘total media universe’ as the beginning and endpoint of analysis (e.g. Ben Compaine, Ken Goldstein, Adam Theirer). But this is problematic for several reasons.

First, it obscures trends at lower levels of analysis, i.e. sector-by-sector and then by category – platform media, content media and online media – before moving to the total network media. We use the “scaffolding method” precisely so that we can pick up on such things.

Second, such conclusions skate over the fact that while concentration levels according to the most sensitive measure – the HHI — fell greatly between 1984 and 2000, they have basically stayed flat ever since, with a significant uptick since 2010.

Third, from the point of view of the CR4 and CR10, there is a distinct u-shape trend over the past three decades. Concentration fell steeply in the 1980s until 1996-2000, when there was a sharp reversal leading to the CR4 being pretty much the same now as it was thirty years ago. On the basis of the CR10, concentration levels were higher in 2012 than in 1984, i.e. the CR10 in 2012 was 81% vs. 76% in 1984.

From this perspective, concentration has grown significantly over time. At best, one might argue that the CR and HHI scores cut in somewhat different directions, or at least the latter are not so pronounced as the former, and thus the results must be seen as mixed. There is little reason, however, to view the current state of affairs and contemporary trends through rose-tinted glasses.

Concluding Thoughts

Several things stand out from this exercise. First, we are far from a time when studies of media and internet concentration are passé. Indeed, theoretically-informed and empirically-driven research is badly needed because there is a dearth of quality data available. Moroever, general developments and the press of specific events – Bell Astral 1.0 in 2012, the resurrected version of the Bell Astral deal that was approved earlier this year, and now the wireless wars in which some claim there is no competition problem in mobile wireless services at all versus those who argue the opposite – demand that we have a good body of long-term, comprehensive and systematic evidence ready-to-hand.

This kind of data is still very hard to come by and data collection for 2012 reconfirmed that at every step of the way. The CRTC still needs a dramatic overhaul of how it releases information and of its website. The underlying data sets included in the Communications Monitoring Report, Aggregate Annual Returns, and Financial Summaries should be made available in a downloadable, open format (also see David Ellis’ series of posts on this point).

The regulated companies themselves must also be made to be more forthcoming with data relevant to the issues, not less as they so strongly desire (see here for a recent example). The CRTC also publishes too much data that does not square with what the companies themselves state in their Annual Reports. Good decisions cannot be made poor data.

The trajectory of events in Canada is similar to patterns in the United States. Concentration levels declined in the 1980s, rose sharply in the late-1990s until peaking circa 2000 and staying mostly flat thereafter. While processes of deconsolidation and vertical dis-integration have taken hold in the US — with the exception of Comcast’s 2011 blockbuster take-over of NBC-Universal — trends in Canada are running in the opposite direction and with the forces of concentration having gained momentum since 2010.

Of course, trends are not all to one side. The assets from the bankrupt Canwest have been shuffled in recent years, and the process is ongoing with Postmedia selling off further papers in the past year, thereby allowing small newspaper publishers to grow (Black Publishing, Glacier). Some significant new entities have emerged (e.g. Blue Ant, Post Media, Remstar, Teksavvy, Netflix, Tyee, Rabble.ca, Huffington Post, a worker-owned TV station in Victoria, CHEK, and a and CHCH in Victoria and another independently owned TV station in Hamilton, CHCH).

The overall consequence is that we have a set of bigger and structurally more complicated and diverse media industries, but these industries have generally become more concentrated, not less. There is a great deal more that can and will be said about what all this means, but in my eyes it means that concentration in no less relevant in the “digital media age” of the 21st century than it was during the industrial media era of centuries’ past.

The next two posts will look at the state of media concentration in the English- and French-language regions of the network media economy, followed by another that will look at the state of media concentration in Canada relative to the US and the thirty countries studied by the International Media Concentration Research (IMCR) project, including the U.S. Germany, Japan, Australia, the UK, France, and so on. The final two posts in the series will profile the top 20 TMI companies in Canada as well as trends with respect to ownership, boards of directors, revenue, profits and debt.

The Growth of the Network Media Economy in Canada, 1984-2012

Cross-posted from the Canadian Media Concentration Research Project blog.

Has the media economy in Canada become bigger or smaller over time? Does the answer to that question, one way or the other, apply across the board, or to only a few of the dozen or sectors that make up the network media economy: i.e. wireline and wireless telecoms; internet access; cable, satellite & IPTV; pay and specialty television; conventional television; radio; newspapers; magazines; music; search engines; social media; internet advertising and online news sources?

Which of these sectors are growing, which are stagnating and which are in decline? To illustrate these trends over the period from 1984 until 2012, this post hones in on rising new media services (IPTV), those that have seen their revenues stay relatively flat over the past few years (conventional television) and those that appear to be in long-term decline (newspapers). I also examine whether the media economy in Canada is big or small relative to global standards.

This post also aims to set down a baseline of data to underpin a series of posts to follow over the next few weeks. Similar to what I have done for the past two years, the next post examines trends within and across the TMI industries from 1984 until 2012 to see if they have become more concentrated over time, or less (for previous versions, see here and here). The post after that zooms in on the top sixteen or so companies with one percent or more market share across the network media in Canada. Such firms account for 86% of all telecom, media and internet revenues. Rank ordered on the basis of revenue, they are: BCE, Rogers, Telus, Shaw, Quebecor, the CBC, MTS, Cogeco, Google, Torstar, Sasktel, Postmedia, Astral, Eastlink, the Globe and Mail, Facebook and Netflix. You can see a past version this discussion here).

In addition to updating our analysis for a complete set of the 2012 data, our goal is to break new ground. This year we do so by adding a new post that examines the state of media, telecom and internet concentration in Canada relative to the preliminary results of a thirty country study by the International Media Concentration Research Project, in which I served as the lead Canadian researcher. There are some surprising results that that smash a few shibboleths while confirming other elements of what we know from past research.

Finally, another new dimension for this year is a break out of data and analysis for the English- and French-language telecom, media and internet (TMI) markets. For the most part, similar questions to those introduced above are addressed about media growth and concentration trends between 2000 and 2012, while the leading firms in both of these regions are profiled in terms of size, ownership, the media, telecom and internet sectors they operate in, and how they each fit into the Canadian mediascape overall. 1

While we cite our sources below, by and large, the following documents and data sets underpin the analysis in this post: Media Industry Data, Media Economy Data, Sources and Explanatory Notes and the CMCR Project’s Methodology Primary.

Canada’s Network Media Economy in a Global Context

Canada’s network media economy has grown immensely over time. Between 1984 and 2012, it nearly quadrupled from $19.4 billion in revenue to $73.3 billion (current $). Adjusted for inflation, the rise was from $39 billion to $73.3 billion last year (2012 $).

While often cast as a dwarf amongst giants, the network media economy in Canada is large by international standards: tenth largest in the world as of 2012, as the overview in Table 1 below illustrates.

Table 1: Canada’s Ranking Amongst 12 Biggest Network Media Economies by Country, 1998 – 2012 (billions USD)

Sources and Notes: OECD Communication Outlook 2013; ITU Revenues 2012. PriceWaterhouseCooper’s Global Entertainment and Media Outlook, 2012 – 2016 (plus 2011, 2010 and 2009 editions) for media and internet. P = preliminary estimate for countries, except Canada. See CMCRP Media Industry Data and methodology primer for Canadian data and analysis.

Canada’s network media economy is obviously small relative to the U.S., at one-twelfth the size. However, relative to the rest of the world, it is amongst the biggest, right after Australia, Italy and Brazil and just ahead of Spain and South Korea.

The growth of the network media economy was especially swift from the early-1990s well into the first decade of the 21st century but like most other countries on the list, it has slowed since 2008, mostly on account of the economic instability that has followed quick on the heels of the Anglo European financial crisis (2007ff). Indeed, worldwide network media revenues fell 5% between 2008 and 2009 and half of the countries listed in Table 1 saw their media economies actually shrink over the following years: the US, Germany, France, the UK, Italy and Spain.

Collectively, these countries’ media economies shrank by around $67.2 billion between 2008 and 2012. Some of this lost ground was regained by 2011, but only on account of increases in the US and France while the media economies in the other four countries (Germany, the UK, Italy and Spain) continued to be smaller than they were before the financial crisis.

In sharp contrast to much of Europe, the US and, less so, Canada, the media economies of Australia, South Korea, Brazil and China have been largely unscathed by the financial crisis. Indeed, these countries and a few others such as Turkey, India, Indonesia, South Africa, and Russia have been going through something of a ‘golden media age’ over the past decade, with most media, from internet access, to the press, television, film and so on undergoing an unprecedented phase of fast-paced development (OECD, 2010).

The Network Media Economy in Canada: Growth, Stagnation or Decline?

As noted above, the network media economy in Canada has grown enormously from $19.4 billion in 1984 to nearly $73.3 billion in 2012 (current $), or from $39 billion in 1984 to just over $73.3 billion last year (2012$). Figure 1 below charts the trends using current dollars.

Source: see Media Economy Data, Sources and Explanatory Notes and the CMCR Project’s Methodology Primary.

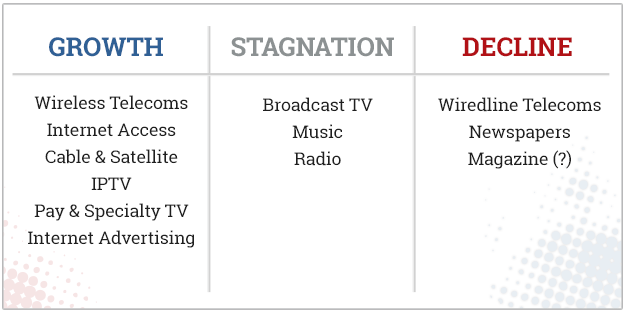

Entirely new sectors – wireless, internet access, pay and specialty tv services, internet advertising – have added immensely to the increase. The most significant source of growth is from the platform media elements (wireless, ISPs, IPTV, cable and satellite), especially after the mid-1990s, but television has also grown enormously regardless of where we start the time line.

Music has also grown slightly, at least once a full measure of all of its subsectors are included – recorded, live, digital/online and publishing – as shown below, while radio has stayed mostly flat. In contrast, wireline telecoms, newspapers and magazines have declined, the first very sharply since 2000 and the latter two gently since sometime between 2004 and 2008, depending on whether trends are looked at from the point of view of real dollars or current dollars.

Table 2 below summarizes the state of affairs across the network media economy as things stood at the end of 2012 in terms of whether each sector covered in this post appears to be growing, stagnating or in decline.

Table 2: The Network Media in Canada: Sectors Experiencing Growth, Stagnation or Decline

The Platform Media Industries

The platform media industries – the pipes, bandwidth and spectrum used to connect people to one another and to devices, content, the internet, and so on — of the network media economy grew from $13.8 billion to $51.5 billion between 1984 and 2012. In real dollar terms, revenue grew from $26.8 billion to $52.5 billion. Table 3 shows the trends.

Table 3: Revenues for the Platform Media Industries, 1984 – 2012

Sources: see Media Economy Data, Sources and Explanatory Notes and the CMCR Project’s Methodology Primary.

Accounting for 72% of revenues, the platform media sectors are the fulcrum of the media economy, as is the case in most of the world. This is why Bell, Rogers, Shaw, Quebecor, Telus, SaskTel, MTS Allstream, Eastlink, Cogeco, etc. are so fundamental to the media economy.

While some might think that the over-sized weight of the platform media in the media economy is of recent vintage, their share of the network media economy in 2012 was basically the same as it was in 1984, i.e. 71-72%, albeit within the context of a vastly larger media economy. This is mostly because of the steep decline in wireline telecom revenues, from $21.2 billion at their peak in 2000 to $15.9 billion in 2012.

As plain old telephone service (POTS) has gone into decline, however, some pretty awesome new stuff (PANS) has come along to more than pick up the slack. Wireless is the best example of this, with revenues skyrocketing after 1996, as Figure 1 and Table 2, above, demonstrate.

Indeed, wireless revenues have nearly quadrupled from $5.4 billion in 2000 to $20.3 billion last year. A corresponding rapid growth in mobile voice and data traffic reinforce the impression. Voice and data traffic were up in Canada 69% and 85% in 2012 over 2011, respectively, with the latter rising considerably faster than the worldwide average (70%)(sources cited here are silent on the other).

The growth in wireless is fast on account of the expanding array of devices that people use to connect to wireless networks: phones, smartphones, tablets, wifi connected PCs, and so on. In short, personal wireless mobile communications are quickly moving to the centre of the media universe. These are the social, economic and technological foundations underpinning the wireless wars that are now in full-swing in Canada.

Some have recently argued that the rate of wireless growth has slowed since 2008, arguing that this is mainly because it is becoming a mature market (Church and Wilkins, 2013, p. 40). Relative to the torrid pace of growth from the late-1990s through the most of the 2000s, this is true. However, it is well known that the pace set during the early commercialization of new technologies cannot be sustained forever. More than this, however, the flattening of growth coincides perfectly with the financial crisis.

This reality simply cannot be ignored. As indicated earlier, revenues for the network media economy worldwide declined between 2008 and 2009 and many of the world’s largest network media economies are still smaller today than they were five years ago (Germany, UK, Italy and Spain), have stalled (Japan and France) or are only modestly larger now than they were five years ago (US, Canada and Korea). Therefore, a modest let-up in the pace of wireless growth amidst such conditions is not surprising.