Archive

Bad News: Proposed Online News Act Trades on Myths and Misconceptions

Last week, the Liberal Government introduced the Online News Act. The Act’s main aim is to redress the dominant market power that Google and Facebook have amassed by building an online advertising system around third-party content, including news, and people’s online activities.

Canada is not alone in taking steps to rein in “big tech”. In fact, this bill is modeled on the News Media Bargaining Code adopted in Australia last year. In addition, public inquiries and regulators in Australia, the European Commission, France, Germany, the United Kingdom, the United States and elsewhere have all concluded that Google and Facebook have monopoly power: the long-term ability to set the prices and terms of trade in the online advertising marketplace (for a running tally of such efforts, see Winseck & Puppis).

This is especially true of Google, which dominates the buying and selling of Internet advertising while also controlling its own online advertising exchange through which much of the buying and selling of advertising online takes place. Those inquiries have also found that the online advertising system is inscrutable to businesses and Internet users alike, coursing with dirty and unreliable data, at odds with European and UK data and privacy protection laws, and free of democratic regulatory oversight (UK ICO, 2019; Belgium DPA, 2022).

As a result of their stranglehold on the key elements of the online advertising system, by 2020, the Google and Facebook had carved out an 80% share of the $9.7 billion online advertising market in Canada.

This is the reality to which the Online News Act, ostensibly, responds. Other governments are taking similar steps to do counteract this state of affairs.

In an ideal world, the Online News Act could help give news media a bigger cut of the dollars and help improve the terms of trade upon which the future of the news media and journalism depend. It could also help give us all a clearer view of the complex black box technical systems upon which the online advertising marketplace is built. Doing so could improve not just journalism but also help to repair the “broken Internet”, an Internet that a small number of international Internet giants have colonized and remade in their image.

In sum, there are good reasons why digital platform regulation could be a good thing. Here’s some of the highlights of what the Online News Act could do well, followed by a list of the ugly parts of the bill that lead me to conclude that it falls far short of its potential.

One, the Online News Act does not impose a link tax on Google and Facebook for linking to news. While France and Spain, for example, have pursued this option, the link tax is a bad idea because it relies on untenable and undesirable changes to copyright law, strikes at a basic technical building block of the Internet (hyperlinks), and rests on the faulty premise that it is possible to attach a clear price to the news. This latter idea has never been possible, and is why we are struggling to find a viable framework to support journalism in the first place.

Second, the Online News Act bill contains a powerful set of tools to strike at the heart of dominant market and gatekeeping power drawn from over a century of antitrust and telecoms regulation history: measures that prohibit Google and Facebook from giving one news provider undue preference over another (or to unjustly discriminate between different services) and a code of conduct that is tantamount to a “fair carriage” regime for all news media services made available over the platforms.

Not only are these measures amongst the best bits of this bill, the Government would do well to put similar measures in the Online Streaming Act, which currently does nothing to deal with these issues of dominant market and gatekeeping power (as I have written elsewhere).

Third, unlike the Australian model which gives a government minister the power to designate which digital platforms will be covered, the Online News Act bill gives the Canadian Radio-television and Telecommunications Commission (CRTC) the power to make the call. The has the obvious advantage of creating a shield against direct political interference by the Minister in charge (i.e. Heritage Minister Pablo Rodriguez, at the moment).

Fourth, the Online News Act opens two options for platforms to strike deals with news media providers operating in Canada, either individually or collectively: the first option encourages voluntary deals; the second imposes final offer arbitration overseen by the CRTC.

In Australia, Google and Facebook have avoided being designated under the News Code altogether by striking voluntary, multi-year deals with the three biggest commercial media conglomerates, one of the country’s two public service media outlets (the Australian Broadcasting Corporation but not SBS), and some smaller regional and local news sources.

The problem, however, is that nobody knows anything about these deals because the Code does not apply to voluntary deals. Did Rupert Murdoch’s media empire (News Corp/Sky) and the country’s two other biggest media groups—Seven West Media and Fairfax Media-Nine—do better than one another or the ABC or any of the smaller media groups? How much of the money agreed upon will be used to hire journalists, expand newsrooms and support international news bureaus versus padding corporate profits? Who knows!

The drafters of Online News Act have wisely made sure that even voluntary deals struck between platforms and news publishers/broadcasters will be subject to review to ensure they are fair and support original journalism versus lining investors’ pockets.

Fifth, that process of review is also a key part of one of the bill’s other potential strengths: its information disclosure and audit requirements. The premise is simple: effective regulation hinges on knowing about the entities to be regulated.

That we have got this far already without Google, Facebook, Amazon, Netflix, Apple, etc. not being subject to such minimal requirements speaks volumes about how much power they have obtained without any real public responsibilities. The Online News Act would help fix that. Furthermore, the idea that regulated companies have an obligation to disclose information to regulators has been a bare minimum part of the regulatory tradition in Canada since the creation of the Board of Railway Commissioners way back in 1903.

So, if there’s all this good stuff in the Online News Act, why should we still put a stake through its heart? Let me count the ways.

For one, rather than trying to counteract the source of Google and Facebook’s market dominance and gatekeeping power, the Online News Act tries to leverage their market dominance for public policy ends: saving journalism. In so doing, if adopted, the act ties the future of journalism to a steady flow of money from Google and Facebook, thereby increasing the dependence of journalism on both firms. It also fails to include one of the best parts of early drafts of Australian Code: a requirement that the US tech giants give news outlets advance-notice of big changes that could up-end the latters’ operations.

Second, the Online News Act mechanics are all about transferring dollars from Google and Facebook to news media operating in Canada through corporatist bargaining arrangements with no seat at the table for rivals, advertisers, experts, academics or anybody else to articulate the “public’s interests” in these matters. In contrast, the public has had a seat in CRTC telecoms and broadcasting proceedings since 1976! Freezing the public out in this way is a profound act of depoliticizing platform regulation and is anti-democratic.

Third, the Online News Act does not tackle the taproots of Google and Facebook’s dominance: i.e. control of the online advertising system, cross-market consolidation of activities across digital markets, and business models driven by the unlimited harvesting of personal information. The last of these points reveals a major reason why Canada has such weak privacy and data protection laws: the big international digital platforms and domestic communications and media firms such as BCE, Rogers, Postmedia, Quebecor, Shaw, Telus, etc. are all joined at the hip in wanting to expand their intensive harvesting of people’s data.

In the context of the Online News Act, and just like in Australia, domestic news media companies don’t want strong privacy and data protection rules for just that reason. Instead, they want a bigger slice of the big data pie. The Trudeau Government is helping to give them what they want with this bill–at the expense of protecting Canadians’ privacy and personal information.

Fourth, while the crisis of journalism that the Online News Act tries to solve is real, the bill is built on a severe misdiagnosis of the problems we face and incessant pleading by Canadian media groups, think tanks, lobbyists as well as the platforms themselves. In fact, the crisis of journalism is the result of a confluence of events that have unfolded for decades, and years before either Google and Facebook had consolidated their dominance in the last ten years. We have reported on these factors for years as part of our research at the Canadian Media Concentration Research Project:

- declining per capita and per household circulation since the early 1970s;

- an orgy of debt-addled consolidation from the mid-1990s until 2010 that put some media firms into bankruptcy (e.g. Canwest, whose broadcasting and newspaper assets were acquired by Shaw and Postmedia, respectively) while leaving many others on shaky financial grounds ever since;

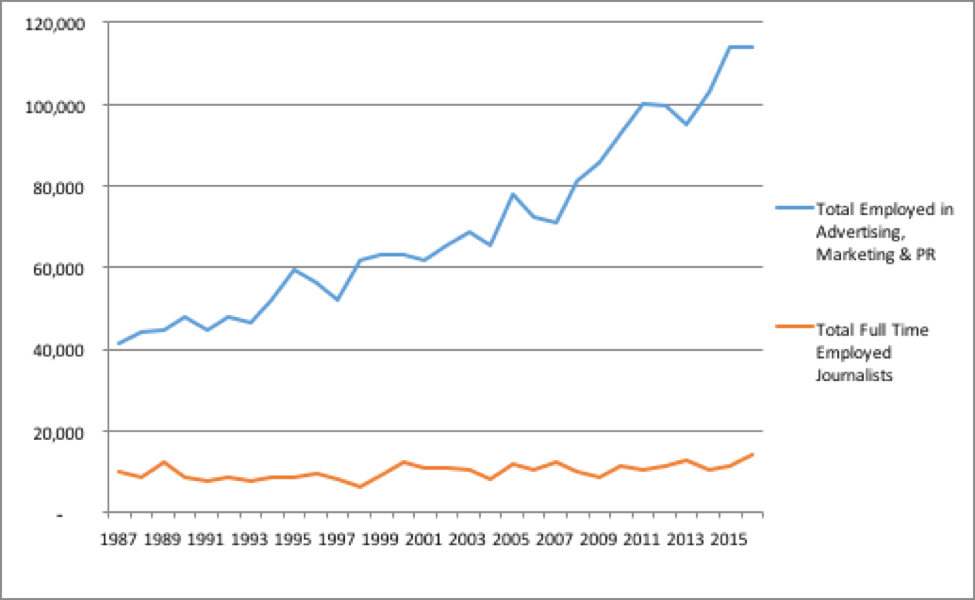

- wild swings in journalist employment levels over the same period and a precipitous drop since 2013;

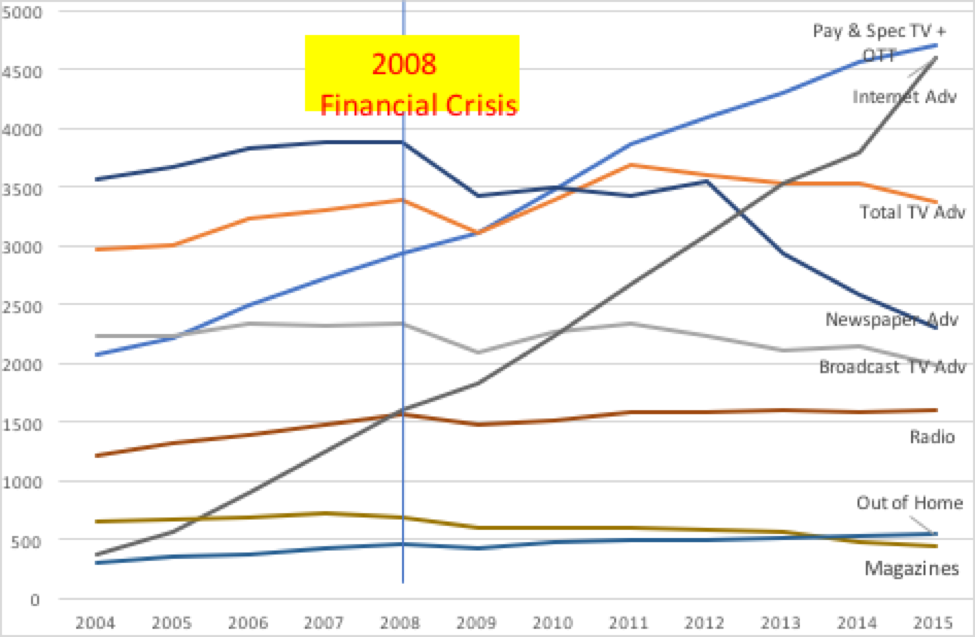

- revenues for newspapers and broadcast news media companies that peaked in the mid-2000s but which have collapsed since, especially after the bottom fell out for advertising spending across the economy after the financial crisis of 2008.

While casting Google at Facebook as the main villains in the piece might make for a good story, it does not reflect an accurate or holistic view of the problems and is misleading. Having fundamentally misdiagnosed the issues, the idea that the Online News Act will solve the problems is wishful thinking.

Fifth, the Online News Act also anticipates a role for the CRTC as a kind of super-regulator. To do that, however, is to ignore the reality that the Commission has proven itself to be ill-equipped to handle its existing mandate, especially under its current leadership. Furthermore, while the bill is said to be about redressing market power imbalances, the CRTC has been extremely timid about tackling such issues in telecoms & broadcasting. Its approval of the Rogers’ blockbuster bid to acquire Shaw’s broadcasting assets—the sixth largest acquisition in Canadian history—last month is just the latest example of this. For it to now turn around and turn the screws on Google and Facebook would be seen as anomalous, even unjust. This is especially so, given that a combined Rogers-Shaw, if approved by the Competition Bureau and ISED, would become Canada’s largest communications and media conglomerate with revenues that would be single-handedly more than three times Google and Facebook’s revenue from Canada, combined.

Finally, while the CRTC’s newfound powers to review deals made under the Online News Act, compel information disclosure and conduct annual audits would be improvements on the “Australian model”, those measures are vague and the details punted to the Commission itself to work out. That problem also plagues the government’s Online Streaming Act (for my analysis of that bill, see here). In both cases, this puts too much trust in the CRTC that it does not deserve and also moves the issues out of the public spotlight and Parliament into the bowels of an agency that has a spotty track record on these matters.

In sum, while the Online News Act has been wrapped in noble cloth, from conception to now, it stands as a massive missed opportunity. Instead of a model to embrace it offers valuable lessons of how not to regulate digital platforms and Internet-based services. Time to go back to the drawing board.

In Defence of the Emergencies Act: Why We Must Put a Stake Through the Heart of the Insurrection Bubble-Wrapped as a Protest (while keeping the EA on a short leash)

The Emergencies Act: Time to Bring in its Never-Before-Used Powers?

Last week, on Feb. 14, the federal government introduced a motion to invoke the Emergencies Act to quell the, then three-week long occupation of Ottawa as well as other blockades set up in Emerson, Manitoba, Coutts, Alberta and the Ambassador Bridge in Windsor, Ontario. As required by the law, Parliament has sat non-stop since (except last Friday) to debate this never-before-used legislation, a law created in 1988 by the then Conservative government of Brian Mulroney. Parliament will vote tonight (February 21, 2022) to determine whether the use of the Emergencies Act is justified and legitimate.

Before the government invoked this extra-ordinary law, discussion was already raging as to whether or not calling on the biggest hammer in the government’s toolkit to deal with threats to national security, the rule of law and public order was justified. A colleague in the Norman Patterson School of Public Affairs (NPSIA) at Carleton University, and a former national security advisor to the Department of Justice, Leah West, questioned whether the high bar for deploying the act had been met. As Professor West stated, the government “must believe the protests rise to the level of a national emergency”. In her view, that high bar had not been met.

While national security law is outside my wheelhouse of expertise, my work over the last three decades on telecommunications, the Internet, communication regulation, privacy, media and democracy, within Canada and internationally, regularly bumps up against such issues. My work as a communications and media scholar, also at Carleton University, as also forever focused on questions about communications, society & democracy. As such, I want to weigh in with a few thoughts of my own in the hope that I have something worthwhile to contribute to the debate.

Here’s the bottom line: While I disagree with Professor West’s provisional conclusions, I do agree that we must be very vigilant that this precedent setting use of the Emergencies Act remains limited in time, targeted in terms of geography, subject to Parliamentary review & snuggled tightly within the confines of the Canadian Charter of Rights & Freedoms.

The big new tools that allow the government to follow the money backing the occupation and to bring crowd-funding services such as GoFundMe and GiveSendGo under the purview of FINTRACK—a part of the financial regulation tools that have been in place for some time—must be given especially close and ongoing scrutiny, as others with expertise in such matters, such as another Carleton colleague from NPSIA, Stephanie Carvin, and others such as Jess Marin Davin, have said (also see Davis, Convoy Finance, Emergencies Act edition).

These commentators have also stressed that, as part of this scrutiny, it will also be essential to closely watch to make sure the use of these tools remain consistent with federal privacy legislation such as the Personal Information Protection and Electronic Documents Act (PIPEDA) and the Canadian Charter of Rights and Freedoms. In this respect, the government should be consulting closely with the Office of the Privacy Commissioner (OPC) to ensure that the privacy & data protection implications of PIPEDA are met.

On this point, it is important to bear in mind that the government already faces a big credibility problem given the Public Health Agency of Canada (PHAC) controversial commercial deal with Telus, the third largest telecoms and mobile wireless operator in Canada, to use Canadians bulk mobile data as part of the public health measures now in place and that many people have grown increasingly impatient with. The government’s decision to play fast-and-loose with such rules has already received a strong rebuke from the head of the OPC, Daniel Therrien. As Therrien has stated, rather than the government (PHAC) consulting with his office, as required by PIPEDA, his office was only informed.

This attempt to do an end-run around the guardrails in place to govern the use of mobile data in the context of public health measures serves as a self-inflicted wound. It also triggered a hastily convened Parliamentary review by the Access to Information, Privacy and Ethics (ETHI) Committee. Serious scholars and observers of Internet surveillance and privacy and data protection issues in Canada, such as Chris Parsons from Citizens Lab at the University of Toronto, Teresa Scassa, Canada research Chair in Information Law and Policy at the University of Ottawa Law School and former Ontario Privacy Commissioner Ann Cavoukian have been highly critical of this short-circuiting of properly informing the public and playing fast-and-loose with the already weak privacy and data protection framework that we do have in Canada. At the very least, this experience shows exactly what the government must NOT do if it hopes to maintain people’s trust in, and the legitimacy of, the extraordinary tools the Emergencies Act will allow it to use.

What is happening is not a protest

With the above in mind, here are my views: First, what had been taking place in Ottawa, Coutts, Emerson and Windsor for three weeks was not a lawful protest but, at is core, and in terms of its conception and management of its execution, an insurrection-wrapped-in-the-trappings of legitimate protest. These are not words to be use lightly. They are, however, justified given that the leadership of these demonstrations and their initial manifesto have openly called for the overthrow of the government of Canada and democracy (since rescinded). As journalists such as Justin Ling have chronicled in this context and over the years, this has been the aim of these events in the insurrectionists’ own words since the outset of the Ottawa Occupation on January 28, 2022.

Ling and others have been tracking extremist groups like the Proud Boys long before they became the far-right Canada First after the government put the Proud Boys on the list of banned terrorist groups in Canada in 2021. The movement whose presence has been on full display in Ottawa since Day 1 is led by far-right extremist who have been active for years and especially since the 2019 Yellow Jackets protests in Canada (ISD, 2021). At a minimum, these groups are anti-state and, after that, the consist of a long list of horribles: racists, neo-Nazis, anti-Muslim, homophobes and others who, far from working within the boundaries of democracy, seek to subvert democracy.

Well-known figures at the core of the unrest are include : James Bauder, Tamara Lich, Chris Barber, Benjamin Dichter, Patrick King. They are opponents of democracy not its champions (Hames, 2019). Canada Unity, another prominent group running the chaos, is led by ex-national intelligence analyst Tom Quiggin, an ex-member of the RCMP and National Emergency Response Team, Daniel Bulford and ex-Canadian military members such as Tom Marazzo . Their skill-sets would seem to pose a grave threat.

Researchers with Antihate.ca have done excellent work for several years chronicling these individuals and the groups they lead, including daily updates since the occupations began.

The movement organizers have money as well as material & ideological support flowing in from across Canada as well as from the US and, far less so, internationally (see here). To be clear: over half of the money has come from within Canada but the vast bulk after than is from the US, followed in a distant second by the UK, a handful of other EU countries, Australia and New Zealand (Cardoso, Globe & Mail).

The big tech billionaire class is also behind the occupation of Ottawa and the demonstrations elsewhere in Canada. This is the case, for example, from Peter Thiel, a co-founder of PayPal and Palantir, as well as part of former President Trump’s inner circle of advisors. Thiel was also a member of Facebook’s board of directors until stepping down earlier this month (Feiner & Levy, 2022). As Thiel emphatically told readers of publication put out by the U.S.-based libertarian think tank, Cato, “I no longer believe that freedom and democracy are compatible.” In Thiel’s view, it is time to get rid of democracy in order to promote the widest realization of individual freedoms.

Elon Musk, founder of Tesla and who also owns and operates the Starlink, the low earth orbiting constellation of satellites that now provides Internet access service to rural and remote areas around the world, including in Canada, hols views that mirror those of Thiel. Musk has been especially vocal in the present context, cheering on the insurrection as if it is merely a benign “Freedom Convoy” and protest. He has also helped to bankroll the unrest (Fortune, 2022).

The Trump connections to this insurrection-occupation-protest are also unmistakeable. Donald Trump Jr. has weighed in many times to give his full-throated support of the demonstrations while condemning the Liberal Government as undemocratic. He has called Canada a “banana republic”, despite overwhelming evidence that it is a strong democracy and typically ranks higher than the United States on various “democracy indices”. Trump Jr. has also shouted from the rooftop the false information that Justin Trudeau is the son of Fidel Castro (see here and here).

Hangers on and former minions of the Trump Administration like Seb Gorka have also piled on (see here, here, here). The hacked GiveSendGo spreadsheet is chok-a-blok full of references to Trump, Trump 2024, January 6, 2022, the false stolen election campaign that brought Biden into office, and on and on.

GiveSendGo List of Donors: Trump Fans Support “Freedom Convoy”

The core group behind this insurrection has bubble wrapped their mission in a disparate array of groups and people with a grab bag of grievances, including about public health measures, for which there can be legitimate basis for lawful protest. There should be a very wide berth for the latter, and there has been, both before the imposition of the Emergencies Act and now. That said, there should be no accommodation for those who openly call for the overthrow of the Government of Canada and the imposition of a provisional junta made up of representatives of the seditionists’ choosing.

It cannot be underscored enough that this is not a protest conceived of and carried out by truckers who have picked up supporters along the way. It has been unfortunate that a great deal media coverage has framed things as being sparked by many people’s legitimate concerns about the ongoing use of public health measures in the context of the Covid-19 pandemic. This has helped to install and reinforce a frame and discursive agenda for how we think about what has been taking place that is highly misleading.

While the insurrectionists are being supported by the far right, Trump supporters and Christian fundamentalists in the United States, the support from rightwing Conservatives in the Conservative Party of Canada (CPC) has been stunning.

Pierre Poilievre, the Conservative Party of Canada’s MP for Carleton, an area just outside of Ottawa, has taken the insurrection-wrapped-in-the-trappings-of-a-protest as opportunity to announce his candidacy for leadership of his party. In a video release one week into the #OttawaSiege that did not hide its opportunistic endorsement of what was already far beyond a legal protest.

Another CPC MP, Candace Bergen has also used the occasion to grandstand for both the demonstrators and her party’s base. She did so during question period in Parliament, for instance, when she hinged a call to demonstrators to “take down the barricades” and “stop disruptive action” while calling on the federal government for an “end to [all public health] mandates. In other words, Conservative Party MP Bergen called on the federal government—a government just re-elected last year explicitly on issues tied to the pandemic-related public health measures—to concede to the demonstrators’ demand in return for an end to the chaos that had been consuming Ottawa and tormenting its citizens for two weeks by the time she made her call.

The second last Conservative Party leader before the ouster of its most recent leader, Andrew Sheer, also gave the the occupation a thumbs up as the siege of Ottawa entered its second week. Sheer’s symbolic support was the Canadian equivalent to U.S. Senator and Trump loyalist Josh Hawley’s famous fist pump to those engaged in the January 6, 2021 uprising against the U.S. Congress and galvanized by the outgoing president’s fraudulent claims that the 2020 US election had been stolen. Yet, here were top members of the Conservative Party in Canada cheerleading on similar forces on the doorsteps of the Parliament of Canada for three weeks by the time that Sheer was endorsing them.

Another former Conservative Party leader, Stockwell Day, was also out rallying the mob tend days into the unrest & extremist minority uprising. Previous members of the CPC who have been recently banished from the party for their rightwing extremist views, such as Maxime Bernier (who has since founded the right wing People’s Party of Canada) and Lanark County MPP Randy Hillier, have also been out in force lending succour to the demonstrators.

Rachel Curran, ex policy director for former Conservative Prime Minister Steven Harper, and now a top Facebook executive in Canada, has also given her blessing to the fun times down at Parliament Hill.

At the provincial levels, the patterns are similar. Doug Ford’s Conservative government in Ontario, for example, was slow to authorize additional policing resources for Ottawa Police and deceptive about the quantum of support when he finally did give it. Instead of promptly and fully meeting calls for 1,800 more police officers from Ottawa Police Chief Sloly and Ottawa City Mayor, the Ford Government engaged in “misleading by design” wordsmithing, as my colleague Josh Greenberg put it, to give the impression that it was doing just that. In fact, the Ford Government offered less than a tenth of that amount but, added up over twelve days, 150 officers per day did amount to 1,800 “officer days” just not the 1,800 officers were needed for a s long as it would take to quell the insurrection.

At the provincial levels, the patterns are similar. Doug Ford’s Conservative government in Ontario, for example, was slow to authorize additional policing resources for Ottawa Police and deceptive about the quantum of support when he finally did give it. Instead of promptly and fully meeting calls for 1,800 more police officers from Ottawa Police Chief Sloly and Ottawa City Mayor, the Ford Government engaged in “misleading by design” wordsmithing, as my colleague Josh Greenberg put it, to give the impression that it was doing just that. In fact, the Ford Government offered less than a tenth of that amount but, added up over twelve days, 150 officers per day did amount to 1,800 “officer days” just not the 1,800 officers were needed for a s long as it would take to quell the insurrection.

That said, Premier Ford is now on board with the Emergencies Act but only just, it seems. In a sidebar to this already tragic story, Chief Sloly, Ottawa’s first black police chief, unexpectedly resigned last week midway through the events.

Two weeks into these events, I also quickly scanned area Ontario MPPs to see where they have stood with respect to the demonstrations and broke them into three groups: 1. those who have condemned the on Ottawa Occupation and blockades of the Ambassador Bridge; 2. those who have gently scolded the demonstrators; 3. and those who have said nothing or openly condoned them. As of February 10, no members of Premier Ford’s government jad explicitly condemned the occupations (see the results here).

In sharp contrast, all of the rest of the Ottawa region’s MPPs from the Liberal and NDP parties had condemned the siege: Joel Harden, Stephen Blais, Lucill Collard and John Fraser.

Other provincial premiers, such as Alberta Premier Jason Kenney, have also been overly solicitous to demonstrators, slow to move and engaged in political gamesmanship with the Trudeau government based on years of ongoing hatred of both Liberals and Justin Trudeau. Kenney has also flirted with hard right conservatives and Trump supporters, such as Senator Ted Cruz, as the photo of the two together helps to illustrate.

At this juncture, it is important to remember that it is now official Republican Party dogma that the January 6, 2021 assault on Congress in favour of overturning the 2020 election that brought President Biden into office constitutes “legitimate speech”. The point here is that acts of insurrection are within the range of acceptable action for these politicians.

That so many members of the Conservative Party of Canada have, at the very least, being playing footsies with such notions, and in some cases embracing those who would seem bent on overthrowing a democratic government, gives rise to the great concern that a large swathe of the official opposition cannot be relied on to uphold the principles of democracy at a time of crisis. This, in turn, feeds into the very basis upon which invoking the Emergencies Act is premised: the threat to public order, national security, the safety of Canadians and the institutions of democracy itself are real and it is no longer possible to count fully on all political parties to stand firm in favour of democracy.

Indeed, as some grass-roots citizens have documented, somewhere around half of CPC’s sitting MPs have offered open support for demonstrators. When half of the official opposition reveals itself to be sympathetic to the events that have shaken the country for the last three weeks and running, it is reasonable to be worried, as the Trudeau Government is, that the institutions of democracy—in this case, the CPC—might not hold. As a result, stern measures are needed and the Conservative Party of Canada have helped to bring about this extraordinary and undesirable state of affairs.

In light of the above, it looks like extremists in the CPC have, at least temporarily, taken over control of the party. It is now time for the Party’s leadership and members to get back control of of the CPC and for conservatives who still believe in democracy to continue to step up. Fortunately, a few journalists who have long been supportive of the Conservatives, such as Andrew Coyne at the Globe and Mail, have been stepping up draw clear blue water between conservatives and insurrectionists.

Crisis of the State? The Ottawa City Government and Police Forces Teeter on the Verge of Collapse

At the city level in Ottawa, Mayor Jim Watson was, for the first two weeks, slow to grasp the severity of the situation. He was also obsequious when dealing with occupation of Ottawa by calling for the federal government to negotiate with the leaders of the demonstrations. Later, just after citizens had taken to the streets to defend their neighbourhoods on their on—as in the #BattleofBillingsBridge—the mayor publicly scolded them for doing so. At the same time, Mayor Watson was striking a deal with the leaders of the demonstration that resulted in some of the demonstrators moving their vehicles out of some neighbourhoods into areas more adjacent to Parliament Hill. The deal was facilitated by Premier Ford’s fixers who had connections to some of the leadership behind the conception and execution of the occupation.

People across Ottawa also watched in frustration and feat that the Ottawa Police proved to be either unable or, frighteningly, unwilling to enforce the law (see CBC journalist Harewood commenting on the situation here; also see here and here). The rule-of-law in many respects was not being upheld around Parliament Hill and adjacent areas such as Centretown where I live for three weeks running. This led to very real questions about whether or not Ottawa Police had the resources they need or, worse, whether they might have been compromised?

That last question, in turn, took on a particular salience given that there had been publicized defiance in the ranks of the Ottawa police on account of the then new Chief Sloly’s attempts at modest reforms designed to root out racism in the force and a small but significant continency of officers opposed to the public health mandates, especially the vaccination requirement for essential workers.

Even after police announced on February 7, that they were cracking down on demonstrators bringing fuel to the trucks idling for weeks on end in the occupied zone, night-after-night I took photos of trucks loading their flatbeds full with gas cans destined for downtown (see here). Other demonstrators carried gas cans in the open, with no repercussions and as they pleased. The downtown turned into a rave scene by the third weekend, replete with a professional sound stage and DJ cranking out the tunes.

It was dangerous to walk in certain parts of the city, to go shopping, to wear a mask, to say the kinds of things that I am writing about here. The threats of violence have been very real, including an attempt by arsonists linked to the demonstration setting fire to large apartment building whose residents had voiced their discontent with the demonstrators incessant threatening behaviour, honking, urinating in public, etc. The attempted arson is now being investigated by the Ottawa Police. For an excellent, first hand account by one of the residents of that apartment building, less than two kilometres from my house, see here.

The neighbourhood grocery store at Bank & Somerset, which serves much of Centretown including many immigrants, low wage earners & refugees who have escaped hell elsewhere only to find it in downtown Ottawa had to close. It’s not been safe to go out and buy food. Another grocery store just a few blocks away from that store, the apartment building mentioned in the paragraph above and Parliament Hill also had to shut its doors.

And when the shops were open, you had to do your shopping in the face of maskless marauders who have refused to follow any public health guidance at all. One result of that was that Ottawa’s biggest shopping mall, The Rideau Centre, has had to close for several weeks. Ice cream shops, vintage stores, restaurants, you name it, all have been held hostage and experienced violence at the hands of those who have occupied our city. At the height of the chaos a week or so ago, Ottawa Police told store owners and people they don’t have the resources to protect them. We were literally on our own!

If you still think there has been little danger, and the my story is over wrought, or that such dangers have been far and in-between, there here’s a crowd-source list that chronicles the impact of the siege on daily life; the harassment, threats, assaults, damage to property (public & private), etc. You can find it here. It is one more example of people—citizens, the public—stepping in to do what “the state” has utterly failed to do, i.e. take steps to help protect the public and maintain public order.

Several city councillors have dithered or been slow to grasp the scale of the assault on our city. In particular, several councillors have led the charge for their constituents since day one: Catherine McKenney (Centretown, and my councillor), Shawn Menard, Jeff Leiper, Mathieu Fleury and Caroline Meehan. They have been incredible in their leadership, brave and resolute.

Mercifully, even if they did not take a role as active and assertive as those just mentioned, most of the others on City council were solidly opposed to what was happening. Only a few seemed to be slow to act or sit on the fence. While Mayor Watson was very slow out of the gate, and took steps that many opposed, he finally seemed to seize hold of the magnitude and gravity of the threat late in the day. Here’s a link to what councillors did what according to my scan of the public statements as of February 9.

Finally, on February 11, “Ontario’s Big City Mayors” finally stepped up to condemn the convoy demonstration (see here). Of course, Canada’s biggest business groups also demanded action once the Ambassador Bridge Blockade gnarled cross border trade. The White House called urging Canada to act & offering help at all levels of the US government. Long before that, the biggest union representing 55,000 drivers and 15,000 long haul truckers in Canada, Teamsters Canada, condemned the “Freedom Convoy” in no uncertain terms.

The Assault on Journalism and the Media

While the Conservative Party of Canada, MPs, provincial conservatives & many politicians at the federal, provincial and city level have failed, there has also been a parallel assault on journalists and journalism. The actions and talk of the former is likely aiding and abetting the latter. This assault on one of the pillars of democratic society—and this from me, a long-standing, harsh critic of the media in this country—this provides clear evidence that the insurrection-cum-occupation/demonstration is not here to improve democracy but to subvert it.

It is one thing to criticize the media with the aim of prodding its members to live up to their fabled role in speaking truth to power and performing their democratic functions. It is something else altogether, however, to vilify journalism so as to open a vacuum into which disinformation, delusional conspiracies and propaganda can pour. Examples of this assault on journalism, the media and democracy are as easy to pile up as leaves in autumn (see here, here & here, for example), but a few here will have to do.

The Canadian Association of Journalists and individual journalists have been sounding the alarm on this front throughout the occupation, but with increasing distress and urgency in the last few days before the police regained control of the city over this past weekend. Lucas Meyer had compiled the list below by February 11.

Canadian journalists now have to be very careful walking the streets of Ottawa and some media outlets, like Canada’s largest private media group, CTV, have had to remove corporate branding from their vehicles in order to safely do their jobs.

Fox News has continued to pour fuel on the flames for the last week or so and brought it’s unhinged approach to media agitation to Canada. It has also encouraged similar events in the U.S.

Last Friday, just as the police were ramping up their efforts to restore public order to the streets of the nation’s capital, Fox News reporter Sara Carter made the incendiary claim that a woman protestor had been killed at the hands of the police.

Only 18 hours later did Carter issue a garbled correction despite authoritative sources and the Ottawa Police itself having quickly declared her incendiary claim to be false. Indeed, instead of correcting the record, she quickly buried her tweet in a pile of other tweets so as to push the false claim and her retraction further into oblivion. By the time, however, the damage had been done: Carters tweet, backed the undeserved authority of Fox News, was cursing, unchallenged, through the right wing of the Internet and on the streets of Ottawa and elsewhere where sympathetic protests in some cities across Canada emerged (see here and here).

Despite one of its journalists spreading a demonstrably false and incendiary claim, Fox News, as far as I know, has still not issued a correction or any kind of statement on the matter. Meanwhile, the damage to us, to police on the street and to democracy continues from Fox News unabated.

This is part for the course for Fox News. What Fox does is not journalism. To understand the enclosed, right-wing network propaganda system that Fox News serves as a hub and megaphone for, in the US, with overflow and influence in Canada and internationally, the Harvard University’s Yochai Benkler, Robert Faris & Hal Robert’s (2018) book Network Propaganda is essential reading. Here’s how they depict the network propaganda system they meticulously describe and explain (note: Fox News off to the right and its links to others to the right of it but not, generally speaking, anywhere else).

It does not play by the normal rules of journalism and media in a democracy. It does not correct errors. It was openly allied with the Trump Administration, serving as its mouthpiece and as a lapdog rather than as a watchdog and independent member of the fourth estate. It serves as a node and megaphone in an enclosed right wing networked media propaganda system offering lots of channels to media outlets—online and legacy—even further to the right but few links to the centre right, the mainstream middle, progressive left and the “far left”.

It’s partners in the rightwing, network propaganda system consists of outlets like Breitbart, the Daily Caller, Gateway Pundit and beyond, many of which have brought their fevered delusions and attempts to discredit mainstream media and subvert democracy to my doorstep on Twitter.

Benkler et. al. stress that we can and do have a rational public sphere capable of doing the work democracy demands BUT they also reveal just how fragile the conditions for a viable public and democracy are today. According to them, roughly a quarter- to one-third of US adults and the network propaganda system centred on hubs like Fox that constantly draw on and pump out extremist ideas from the far-right fringes into the body politic.

This sizeable slice of the US population and their media have, essentially, checked out when it comes to basic precepts of democracy, i.e.:

• respect for evidence,

• pursuit of understanding,

• correcting errors when identified,

• provding independent, critical knowledge/reporting,

• baseline trust in institutions of democracy, experts, science & fellow citizens still persists, etc.

That big slice of the US population no longer operates in a manner consistent with a culture of democracy. What we have been seeing in Canada and the streets in Canada in these past few weeks—but building up over the past decade or more, while always existing underground—is smaller and still less entrenched and vociferous. As a guestimate based on a rough-and-ready reading of recent public opinion surveys, the proportion of the Canadian population checked out from democracy is probably around half the rate in the U.S.. In other words, there are probably between 10-15% of Canadians who no longer believe in democracy and act accordingly. They are the source of the inarticulate grunts of FREEDOM that we have heard from the occupied streets of Canada’s capital for the past three weeks.

This coverage from Evan Solomon for CTV’s Power and Politics and from Jordan Klepper of The Daily Show captures the drift of things. The people that they spoke to, in a literal sense, seemed to have no words. A discourse of democracy is beyond them. Why this is so is complex, but it is rooted in a half century of the neoliberal conquest of society & neglect of some minimum sense of economic justice, steps to ameliorate wage stagnation & widening income and wealth inequality, quality education for all, an appreciation of ‘the public’ and a generous view of public goods.

Disenfranchised at one end & prioritizing self-aggrandizing accumulations of wealth freedom at the other (ala Thiel’s freedom versus democracy), here we are: a stunted public incapable of self-governance because while they’ve talked for so long–a half century–nobody has listened & helped to translate their dreams into a viable political project and reality.

At the same time, it would be a colossal mistake to believe that everybody who has taken part in, or supported, this insurrection-cum-occupation (pretend protest) is stupid. They are not. I will return to that issue some other time.

I digress. The impact of the network propaganda system cuts across class. As discussed above, a slice of economic and political elites are driving the corrosive behaviour that has brought to where we now stand and democracy teetering on the brink and our streets filled having been filled with menacing threats. For the rest of us who have little desire for the nihilistic fantasies of this anti-democracy group we now face major conflicts and clashes, within our own families and amongst friends and colleagues, as we watch people we thought we knew float off the deep-end (but with memories of how they might have become this way.

For a long time, the goings on in Parliament and key segments of the media in Canada have also jhad a very corrosive impact, as the views of extremists get amplified, broadcast & normalized. This is the game of the far right vying for the soul of the Conservative Party of Canada right now, as well as the editorial pages of the National Post, the Postmedia chain of papers in major cities across the country and Sun Newspaper chain (also owned by Postmedia).

Citizens, Activists, Community Groups, Hackers Begin to Take Matters & Public Order into their Own Hands

As the state collapsed around them, and the assault on the media and routines of daily life continued unabated, and even amped up in the second and third weeks of the occupation, people, citizens and activists began to take matters into their own hand.

I saw that two weeks ago when joining hundreds and maybe more than a 1000 of Ottawans in the counterprotest march down Bank Street from Landsdowne. The next day many of the same people and many others joined a group of women to block a convoy heading from the Occupation’s organizational centre at Conventry Road to Downtown Ottawa. Over the course of the next nine hours, in the great #BattleofBillingsBridge, we blocked their path and forced them, with the aid of the police, to return back to where they came from, one-by-one, and only after they stripped their vehicles of flags and other pro-occupation symbols (see here, here and here).

They were supported by several city councillors and an area MPP, all of whom’s names you’ve been introduced to earlier: Catherine McKkenney, Shawn Menard, Jeff Leiper, Mathieu Fleury and Joel Harden. But it’s been people who have been taking to the streets to get them back under our control and out of the hands of marauding thugs in pick-up trucks. Zexi Li and a team of lawyers led by Paul Champ also emerged as something like town heroes when they by getting an injunction to silence the incessant honking from big rigs throughout the downtown core before the city and province seemed to have lifted a finger.

Resistance and citizens taking matters into their own hands have also been aided by some pretty far out and brave acts by the RamRanchResistance. They hacked the chat rooms and social media services of the demonstrators and filled them with videos and a gay porno music soundtrack that must have drove the demonstrators crazy. Hackers obtained the donors list from GiveSendGo and distributed it to other researchers but within a short of time the list was being widely shared (see here).

Every movement needs its spectacles and theatre. The occupation forces knew that and had their’s. This was our’s even if came a bit late in the day.

So, why did the federal government have to step in and reach for the Emergencies Act? Because, going into the third week of the occupation its own inaction and the complete failure and, indeed, collapse of political and policing authority at the city and provincial levels was a palpable threat to the safety and security of both the citizens of Canada and the state itself.

With citizens, activists and everyday neighbours beginning to step in to fill the void where the state had failed, things were now becoming even more dangerous. Somebody had to act because now conditions were becoming explosive, just as the insurrectionists at the core of this slow motion coup-wrapped-in-a-legit-looking demonstration/protest have wanted all along. It’s part of their nihilistic fantasies.

Stick your head in the sand if you want to, but the above provides an accurate portrait of the reality of living in Ottawa, the capital city of one of the strongest democracies in the world, for three weeks running . . . before the announcement of the Emergencies Act last week and this week’s assertive moves by Ottawa police, backed by the Ontario Provincial Police (OPP), the RCMP and officers brought in from across the country restored some semblance of law and order. In case you haven’t been paying attention for the last decade-and-a-half, democracies have fallen on very hard times and been rolled back in many countries (see The Economist’s annual surveys on the state of democracy, for example). That distemper is now in our streets and it is time to take resolute steps to protect the democracy that we have with an eye to rebuilding a new, stronger and more inclusive democracy in the days, months and years ahead.

Back to the Law, or the Return of the State, the Emergencies Act and Democracy

Now, back to the legal question that I started with. The point underpinning everything to this point is that the threats are very real, not just to the state itself but to us, the citizens of Canada & society. This is why I respectfully disagree with my colleague, Professor West and all others who oppose the invocation of the Emergencies Act at this time.

Participating in these events, for me and others personally, has been dangerous. The treat of serious injury is real and it is chilling. I have not been able to walk my streets freely with the freedom to speak my mind freely and openly, to associate with others, to wear a mask and to move about without fear for close to a month.

I have had death threats and I have had menacing tweets flooding my timeline for weeks. Here’s a sample of some of the most vile and odious (see here as well).

This is not freedom, nor is it normal in a democracy. It is tyranny of an authoritarian kind, as Hannah Arendt would probably say (see Williams, 2017 & Arendt, 1951/2004).

I am not alone. My colleagues report receiving much the same.

I have reported all of these instances of threats to Twitter and then blocked all of the accounts that had been tweeting them at me. My success rate for getting Twitter to find that these tweets violate their terms of service, however, is roughly a third and I have no idea how they have arrived at their decision to take something down or leave it up.

I suppose we might take some cold comfort that Twitter is at least doing something and that most of these accounts appear to be fake, sock puppet accounts run from troll farms in far-away places (see Ben Collins on this point in this context). That there is LIKELY no real person behind most of the threats is helpful, I guess, but barely.

These threats are why the government is actively pursuing Online Harms legislation as we speak (to track the Online Harms Consultation, see here). I vehemently disagree with the tack being taken with respect to online harms, and still do even after all this.

That opposition is based in a lot of things, including that the concept of online harms is too woolly and unbounded, that the imagined role of online content services like Twitter, Youtube and Facebook in being able to execute what’s being asked of them is unlikely and for two other huge reasons: first, because I believe in free speech, as set out in the Charter and, second, because I think the real problem stems from the fact that so much of the rot that we are concerned about starts at the top, especially within the Conservative Party of Canada, while at “the bottom” we have fifty years of pushing the marketization of society and the stripping away of society so that those tearing up our streets have had no place to go. Until we take of all those things, online harms is little more than lipstick on a pig.

As an aside, if you are interested in my views on the Liberal government’s proposals on regulating Internet content services, this post on the Online Streaming Act will give you a flavour of how strongly I stand in favour of free expression rights and remain critical of this government’s proposals with respect to these matters.

Back to the point: people are now having to take matters in their own hands at the risk of very serious bodily harm at the hands of those who had seized control of our lawless streets. The threat is real. Respectfully, while Professor West might still be able to claim that the current state of affairs does not meet the formal legal and technical requirements of the Emergencies Act, I am not sure if she and others opposed to its use have the full scope of the situation in view.

In fact, I wonder if opponents of the use of the Emergencies Act have adopted an overly formalistic view of the technical facts of the law that effectively obscures the reality that law is always a mix of such facts and procedures on the one side and social and political reality and the need to anchor law in legitimating norms, on the other. On this point, I’m channeling Jurgen Habermas’ (1996) Between Facts and Norms, a magisterial treatment of the nature and role of law in liberal capitalist democracies.

However, I also agree that we must be very vigilant that this precedent-setting use of the Emergencies Act created by the Conservative government of Brian Mulroney in 1988 remains limited in time, targeted in terms of geography, subject to Parliamentary review and snuggled tightly within the confines of the Canadian Charter of Rights & Freedoms. State powers once established and locked in place are very hard to rollback.

That will be our challenge in the days, weeks & maybe months ahead. Now, the goal is to recognize that the uprising was fairly easily quelled once all levels of government got their acts together and there is little doubt that the Emergencies Act hanging in the winds played a vital role in getting the streets clear and some sense of order back. The clear and present danger to my life, my freedoms, our way of life and to Canadian democracy was relatively swiftly pushed back with an absolute minimum of blood shed (as far as I know).

In light of all this, I say pass the Emergencies Act tonight. Then keep it on a very short leash. Bring on the legal challenges now being mounted by the Canadian Civil Liberties Association. I am all for that. Critics? Let a thousand critiques bloom. For now, I’m off to the puppy park, glad to see a minimal police state doing what needs to be done so I do not have to live in the tyranny of a bunch of insurrectionists bubble-wrapping their attempts to overthrow democracy and the state in the guise of legit protest.

Still not dead: Why we need to kill Bill C-11, the Online Streaming Act, and start over

How fitting that the day after groundhog day, here we are once again assessing whether Bill C-11, the Online Streaming Act (or Broadcasting Act reform bill) introduced yesterday, is any better than the one that failed to become law last year? The short answer is, there have been some important improvements to address critics’ concerns, but there is still a long way to go.

The biggest problem stems from the fact that the bill’s drafters and backers are still trying to see the Internet-centric communications and media environment through yesteryear’s broadcasting prism. Moreover, the bill is all about content, and says nothing at all, really, about concentration in digital markets or the surveillance capitalism model that has, in essence, wrecked the Internet.

The Good

On the surface, the aim of Bill C-11, the Online Streaming Act, is to bring influential streaming television, film and music services such as Netflix, Crave, Disney+ and Spotify under the Broadcasting Act and the authority of Canada’s communication and media regulator, the Canadian Radio-television and Telecommunications Commission (CRTC). That was the stated goal of C-10 and it is still the stated goal of this year’s version. In some ways, it would be easy to say that not much has changed between the new bill and previous versions of it, i.e. Bill C-10. And if that was the case, then I could just send you off to read what I wrote about the last version (see here and here). That would be too easy, not least because there are three important improvements to what was previously on offer but also a basketful of problems held-over from the last bill and with some new ones thrown in just to make things interesting.

First, the headline change is that the bill restores the explicit exemption for people who use social media services from it—and the CRTC’s—reach (sec. 2.1) and for the content (redefined as programs) that they upload to such a service (sec. 4.1). On the surface, this responds to the firestorm of criticism ignited around questions of free speech when a similar clause was removed midway through debates over C-10 (also see Michael Geist on this point).

The technical briefing notes distributed by Canadian Heritage emphasize the point, “Regulation will not apply to individual creators, streamers or influencers or social media services themselves in respect of the amateur programs posted by their users” (DCH, 2022, p. 8, emphasis in original).

Second, the bill does not make social media services responsible for the content people make available through online services (but see the exceptions below) (sec. 2.2). Bill C-10 had no such measure and some groups like Friends of Canadian Broadcasting, amongst others, have been pushing the idea that platforms’ should be responsible for people’s expressions on their services just like broadcasters are responsible for the editorial choices they make and the content they commission. In other words, while social media companies might be media companies—rather than just ‘mere conduits’ or platforms—they are not broadcasters, with all the means with respect to exercising control and responsibility over what people do and say on their services.

This is a good thing. It is an important improvement because it minimizes concerns that making Facebook, Twitter, Tiktok, Youtube, etc. responsible for what people do or say on their service could have a chilling effect because such services, keen to avoid liability for users’ speech, would have legal and business incentives to quickly take down risky speech rather than just speech that is not protected by the Charter. Doing so would not just minimize their risk, it would also minimize costs and be good for business.

Online streaming services such as Netflix, Crave, Amazon, Disney+ and Spotify, however, as online broadcasting undertakings (see below), will be responsible for programs commissioned by and/or distributed on their services. Conceivably, this would give the CRTC a role vis-à-vis Spotify and the current, red-hot controversy over its hosting of rightwing provocateur Joe Rogan (sec. 4a). This follows from, as we will see in a moment, the fact that Spotify would fit the definition of an online broadcasting undertaking. The upshot is that speech would be regulated in such instances but within an explicitly articulated legal and regulatory framework and against the backdrop of the Charter protections for freedom of expression and the press.

I believe that this will be helpful. It democratizes decisions that are now the exclusive prerogative of massive, international businesses who, in many cases, have no ties or particular obligations to the citizens and people that live in the countries they serve and feel the brunt of decisions they make.

This points to the third major improvement in the new bill over its predecessors, namely that Bill C-11 now gives pride of place to freedom of expression and values of the free press by putting it at the top of the list of the Broadcasting Act reform bill’s objectives (sec. 3(a)). Given the case just outlined—and the realities of the world around us at this fraught time in the history of democracy in general as well as Canadian democracy in particular–I believe that this is a very good thing.

The Bad and Ugly

These are significant improvements. However, there’s much more than first meets the eye. The upshot of these limitations, as we will see momentarily, is that this bill still falls far short of what is needed from the get-go in terms of creating a new set of public interest-based Internet services regulation fit for a democracy. This is largely because the regulatory framework the bill proposes still tries to force-fit issues arising from the Internet, streaming services and social media platforms into the broadcasting mold. It’s a cramped and poor fit.

The first indicator of this arises in the definitions set out at the top of the bill. First up in this regard is the addition of “online undertakings . . . for the transmission or retransmission of programs over the Internet for reception by the public” as a new and distinct class of broadcasting undertakings (sec 2.1). As a result, instead of flexibly tailoring a legislative response to the rise of new and influential streaming audio, television and film services such as Netflix, Crave, Disney+ and Spotify in a manner that reflects developments over the past three decades, the Bill tries to bend these new entities and ways of organizing the media business backwards into the definition of broadcasting.

It is also worth noting that, like its predecessor, the bill sweeps a whole new category of media into its ambit: music services. Sure, radio broadcasting is where broadcasting regulation started back in the 1920s and 1930s, but stand-alone music services, record companies and music stores were never covered. This bill would change that.

Second, while the Bill, to its credit, as we saw earlier, explicitly excludes people who use social media from its reach, the Act redefines all forms of expression/content/speech that people upload and make available over an online streaming service or social media platform as a “program”. So, while individual social media users will not be directly regulated (but see below), their expressions, pictures, messages, life history, etc. will now be defined as a broadcasting program and in some cases regulated as such (see DCH, 2022, p. 11). In other words, while individual users (speakers) are out, it appears that the content of their expressions are within the reach of the Broadcasting Reform Act while whether or not they will be specifically regulated by the CRTC will turn on a number of criteria set out in the bill.

The problems in this respect are two-fold: first, this exercise in redefining a wide range of human expression in the confined box of “broadcasting programs” threatens to smuggle in through the backdoor what the bill explicitly says is being excluded: expressions/content that people upload to a social media service. The slippage in the technical briefing notes handed out yesterday, and Minister Rodriguez’s comments in the media between a clear and emphatic emphasis on how social media users will be excluded from the bill—and the CRTC’s—reach without a consistent and similar emphasis on how their expressions/speech/content, and the re-labelling of such as “programs, will be treated further muddies the waters on this issue.

Philosophically, recasting the entire range of human expression and activity now conducted online through the digital platforms as “programs” seems technocratic. Doing so, wittingly or unwittingly, strips the questions of speech and expression of the normative values that flow out of the long-standing discourse over freedom of expression and democracy. Moreover, and in simple terms, it is unclear what purposes redefining speech and expression in this stunted, technocratic way will ultimately serve. It is worth noting that such efforts to confine the full range of expression into the cramped confines connoted by the concept of a “broadcasting progam” is new and seems wrong on the face of it.

In other words, while individual users (speakers) are not covered by the proposed law, it appears that the content of their expressions—redefined as programs—are within the reach of the Broadcasting Reform Act but whether or not they will be specifically regulated by the CRTC will turn on three specific criteria set out in the bill. In fact, the new version of Broadcasting Act reform bill strives to limit the potentially far sweeping reach of this new definition by being explicit that only programs—that is, all kinds of expression uploaded to a platform—that meet the following three criteria will fall under the reach of the CRTC:

- generate revenue;

- are broadcast or made available on more than one service that is either licensed by or registered with the CRTC;

- have some kind of an international service identifier tied to it, such as ISO number (sec 4.2(2).

The intent of these criteria is to give the CRTC the tools that it needs to distinguish between the programs that will fall under its authority versus those that will not. The goal is to distinguish between professional, commercially-driven media content and content creators versus everybody else who will be left untouched. The distinction itself is consistent with the European Union’s Audiovisual Media Services Directive, which much of this bill’s design and justification rests on, but both, these specific criteria and the line that they are supposedly meant to drawn between professional, commercial programs versus people’s everyday online activities, are muddled. Too many conceptual contortions are required just to follow the plot and to serve as a steady guide.

To help assuage such concerns, CRTC chairman Ian Scott has repeatedly said that the Commission has no interest in regulating social media, but he has also prevaricated by pointing to just how broad the existing definition of broadcast program already is. In other words, Scott is saying that Commission could already do what this bill contemplates but won’t because it does not want to. That is not good enough. His assurances, moreover, rings hollow given statements made by the Executive Director, Broadcasting, at the CRTC, Scott Hutton, to the ETHI committee in 2018 that suggest otherwise.

Once a “program” delivered over Internet meets those three criteria, the specific obligations that an online platform service (online broadcasting undertaking) would have to meet are, as with the last bill, left to the CRTC to decide. Things that it would be able to decide on include:

- the amount of Canadian content in an online streaming services catalogue.

- the amount of money they would have to invest in Canadian programming.

- promote the accessibility of programming in English and French and in terms of accessibility for people with disabilities (see sec 3(4).

C-11 also extend the CRTC’s order making power to these online content services (sec. 7(7). It would also give it the power to imposed “administrative monetary penalties” (AMPs) (Part II.2).

The major problem in all of this is that Bill C-10, like its predecessor, punts far too much power and rule-making authority to the CRTC. Moreover, it does so precisely at a moment in time when neither the current chair or the Commission writ large seem to have the resources, inclination or leadership to cover the existing mandate to effectively regulate telecoms and broadcasting in the public interest. Adding additional matters on to the CRTC’s remit in this context is inappropriate.

In fact, just as the liberal government was setting up to reintroduce the new bill and extend the CRTC’s regulatory authority over online video and music services, as Fenwich Mckelvey, Brenda McPhail and Reza Rajabuin observe, in a recent decision that could have opened the door for greater public oversight of algorithms and artificial intelligence capabilities being deployed by Canada’s telecoms operators, the CRTC slammed the door shut on that prospect while also making it next-to-impossible for independent scholars to effectively know the crux of the issues at stake and, thus, to effectively participate in the proceeding, period.

Moreover, the CRTC’s ability to take on new tasks is compromised by the fact that its own data on online content services over the past several years has been badly flawed and based on cherry-picked evidence that, in hindsight, has been revealed to be grossly over-stated, seemingly as part of its own ongoing campaign to expand its turf in exactly the way Bill C—11 contemplates. The Commission has acknowledged as much by restating previous year’s data for several years running now (see CMCR Project, 2021, for example). In short, the Commission now lacks the credibility and trust upon which the successful execution of the tasks that Bill C-11 assigns to it depends.

The Neglected/Ignored

Crucially, we must also ask what is missing from this bill? Five things stand out.

First, this bill lacks clear thresholds for determining what’s in and outside its scope. This is unfortunate because establishing clear thresholds based on revenue, the size of the user base and market capitalization, for example, are headline features of the European Union’s Digital Markets Act and Digital Services Act as well as a suite of platform regulation bills now before the U.S. Congress (see here). In the EU, the proposed legislation is very clear that it only covers a well targeted set of “very large online platforms” (VLOPs), while in the U.S., current bills before Congress speak of “covered platforms”.

This is low hanging fruit and should have been included in Bill C-11. Not only would it have clarified some of the muddled line drawing exercises and definitions outlined above, it would put the CRTC on a shorter leash and hold it more accountable to Parliament—a formal requirement in terms of democratic legitimacy.

Second, the bill maintains no clear and robust information disclosure obligations that would apply to the services brought under the Act and CRTC authority. Doing so would help us—the public, academics, parliamentarians, journalists, and regulators—to better understand the streaming services & online platforms activities that now operate in Canada and their decision-making processes. Without such obligations, these services remain a blackbox.

Third, and relatedly, Bill C-11 continues to feature a stunted view of “discovery” that is primarily about pushing more Canadian content (Cancon) in front of more Canadians’ eyeballs. Instead, it should have looked toward a more progressive view of “discoverability” along the lines that, for example, Fenwick McKelvey, communication studies professor at Concordia University, has articulated. In this more progressive view, instead of forcing CanCon to rise to the top, as the broadcasting-driven Bill C-11 does, discoverability would focus on opening the complex technical communication and media systems that increasingly influence access to and the presentation of expression online to greater public scrutiny and regulatory oversight. Instead, C-11 retains the stunted Cancon view of discoverability and, worse, the bill back-peddles on the issues of greater algorithmic transparency and information disclosure by introducing new limits on the CRTC’s access to the algorithms and source code at the heart of the online streaming and platform services (sec. 10(8)).

Fourth, the flipside of the lack of accountability and robust information disclosure obligations, C-11 does nothing to establish privacy and data protection rules. As such, the legislation not only neglects a critical moment in which it could begin to lay down strong data and privacy protection rules across the many different aspects of the online digital environment, it effectively puts its thumbs on the scale in favour of the surveillance capitalism model upon which these services are based.

Fifth, not only does C-11 add further momentum to the surveillance capitalism imperatives that are the taproot of so many of the problems that now characterize the digital online environment, it does nothing to address issues of market dominance and anti-competitive conduct. In other words, by fixing its eyes on content issues, the bill accepts the status quo and leaves problems of digital market dominance where it does exist unscathed.

Take, for example, the recent contretemps in the U.S. that saw a classic goliath versus goliath battle between Google’s Youtube subscription service and Disney (Bloomberg, 2021). The battle had all the hallmarks of a classic cable industry fight over the terms of retransmission, including a black out on programming when Disney withdrew its content from the service. The case raised critically important issues about the conditions of carriage that are at the heart of what all “broadcasting distribution undertaking” (aka, BDUs, or in simple language, cable television, in everyday parlance) are obligated to do and how disputes between them and programs rights holders are to be handled. The Broadcasting Act reform bill, however, is completely silent and seemingly oblivious to such issues.

As app stores, such as Google Play and Apple’s App Store, as well as digital platforms, such as Amazon Prime Video, Crave, Netflix and Apple TV and iTunes, operating in a way similar to cable television, IPTV (internet protocol television) and direct-to-home satellite providers (all BDUs in official CRTC-speak), these issues will become more important. That they are ignored here is, while not surprising, is a big mistake and a fatal weakness of C-11, like its predecessor. In sum, just as the previous bill did, C-11 leaves the problematic system of market power & surveillance capitalism intact.

These issues were, in fact, taken up in the Broadcasting and Telecommunications Legislative Review Panel’s Canada’s Communication Future (2020) (see chapter 2, in particular). The fact that they are absent from C-11, to my eyes, stands as an index of just how one-sidedly fixated on broadcasting and content issues this bill is, and the extent to which the Canadian cultural policy community continues to have a strangehold on the government’s policy and regulatory agenda. That the drafters of C-11 have ignored these issues is an index of a bill that still, for the most part, has its head stuck in the sand.

To sum up, the Liberal government had an opportunity to go back to the drawing board & really get this opening plan in its emerging Internet services regulation right. It had/has a huge opportunity to align this agenda with what a new generation of public interest, Internet regulation fit for a democracy should look like. It made some baby steps in this direction, as we saw above, but it did not engage in thorough-going overhaul that is needed. As a result, C-11 stands as another missed opportunity.

Time to Kill Bill C-10, An Act to Amend the Broadcasting Act

Bill C10, the Broadcasting Act reform bill, has set off a firestorm of controversy. Originally presented as being all about revising the Broadcasting Act to bring online audio and visual streaming media services like Netflix, Crave, Spotify, and so on into its reach, the bill has taken on far wider and worrying prospects.

This is because Bill C10 treats any expression online that is aggregated by the likes of Google’s YouTube, Facebook, Reddit, TikTok, and so forth as if it’s a broadcasting program and should be regulated as such. The bill’s defenders are correct that it does not directly subject individual Canadians to CRTC regulatory oversight. However, through a process akin to alchemy that turns people’s everyday expressions into programs when uploaded to a platform, people’s expressions (content) will become subject to CRTC authority. It also makes “content aggregation” the baseline for defining a broadcaster, similar to how ideas about spectrum scarcity (among other things) were used to justify broadcasting regulation in the 20th Century. The very act of “content aggregation” is then seen to magically transform a platform into a broadcaster. Lastly, all of this would bring digital platforms under the CRTC’s supervision, as if it is already not struggling to meet its mandate given its current resources and leadership.

To be crystal clear, I agree that we need a new generation of digital platform and Internet regulation. In fact, liberal democracies worldwide are actively engaged in efforts to this end. The Liberal Government, in other words, is not alone, although its botched approach is something to behold. Indeed, these efforts by liberal, capitalist democracies are so extensive that my head has been spinning just trying to keep track of them all. To help fix that, Manuel Puppis and I decided last year to maintain a document just to keep track of them all. You can find the list now approaching 100 items here.

I fully support the idea that digital platforms and Internet-based content, applications and services can and should be subject to democratic oversight and rules made by Canadians through legitimate processes versus letting the rules be set unilaterally and unaccountably by global Internet corporations based in the United States or anywhere else. We need a new generation of platform and Internet regulation that tackles the extraordinarily high levels of concentration—in online advertising, app stores, search, social media, online video services, etc.—that now characterize vast swathes of the Internet. In most of those cases, the dominant players are tightening their grip rather than seeing new competition emerge.

Second, we also need strong rules designed to open up and subject the digital platforms’ blackbox technical system to regular regulated audits. We need such rules so that we can “discover” what’s inside the platforms’ blackbox, to shed light on how these complex technical systems work so that we can spot the potential for ‘systemic risks’, and to make sure nothing fishy is going on that could allow the Amazon, Netflix, Facebook, Google, Bell, Rogers, Quebecor, Shaw, Telus, etc. an unfair advantage over those who use the same platforms to offer competitive services, to understand how billing systems work and ensure that 3rd parties offering their wares on these platforms are getting a fair shake (e.g. YouTube and TikTok creators)(Mckelvey, 2020).